March 2025: Institutional Chain Reaction

Research Team

Last Updated: 3/31/2025 | 14 min. read

Crypto valuations were down slightly in March 2025, but the month included many signs of accelerating institutional activity — continuing a chain reaction of events that started with the U.S. election in November. After the recent shifts in U.S. crypto policy, institutions seem to have sufficient confidence in the medium-term outlook to make sizable investments in the digital assets industry.

Our market capitalization-weighted Crypto Sectors index declined 5% during March, while Bitcoin’s price fell 2% (Exhibit 1). It was a challenging month for traditional assets as well: U.S. equities declined, with weakness led by large-cap tech stocks and cyclicals; global fixed income markets also produced negative total returns. Meanwhile, the U.S. Dollar depreciated versus the Euro and the price of gold. Historically, the price of Bitcoin has had a positive correlation with broad equity indexes and a negative correlation to the value of the Dollar.[1] Therefore, the mixed results for crypto in March — when both equities and the Dollar declined — look broadly consistent with historical correlations.

Exhibit 1: Crypto valuations were approximately unchanged in March

Growing Conviction

Although it was a relatively quiet month from a valuations standpoint, the torrent of news on institutional activity underscored the ongoing shifts across the digital assets industry.

First, deal activity has increased. Crypto exchange Kraken announced that it had acquired futures trading platform NinjaTrader for $1.5bn — the largest crypto M&A deal to date.[2] The move will allow Kraken to offer regulated crypto futures and other derivatives in the U.S. market and overseas. At the same time, Bloomberg reported that Coinbase is in advanced talks to buy crypto derivatives platform Deribit — the leader in crypto options trading — which could be an even larger transaction based on recent valuations for Deribit.[3] There were also a few sizable venture rounds during the month, including a $400mn investment into the TON Foundation from Sequoia and others, as well as a $2bn investment in Binance from Abu Dhabi sovereign wealth fund MGX.[4] Over the last two quarters, Grayscale Research estimates (using data from Messari) that total crypto industry fundraising reached about $10bn, compared to $3.5bn over the preceding two quarters (Exhibit 2).

Exhibit 2: Higher fundraising activity since U.S. election

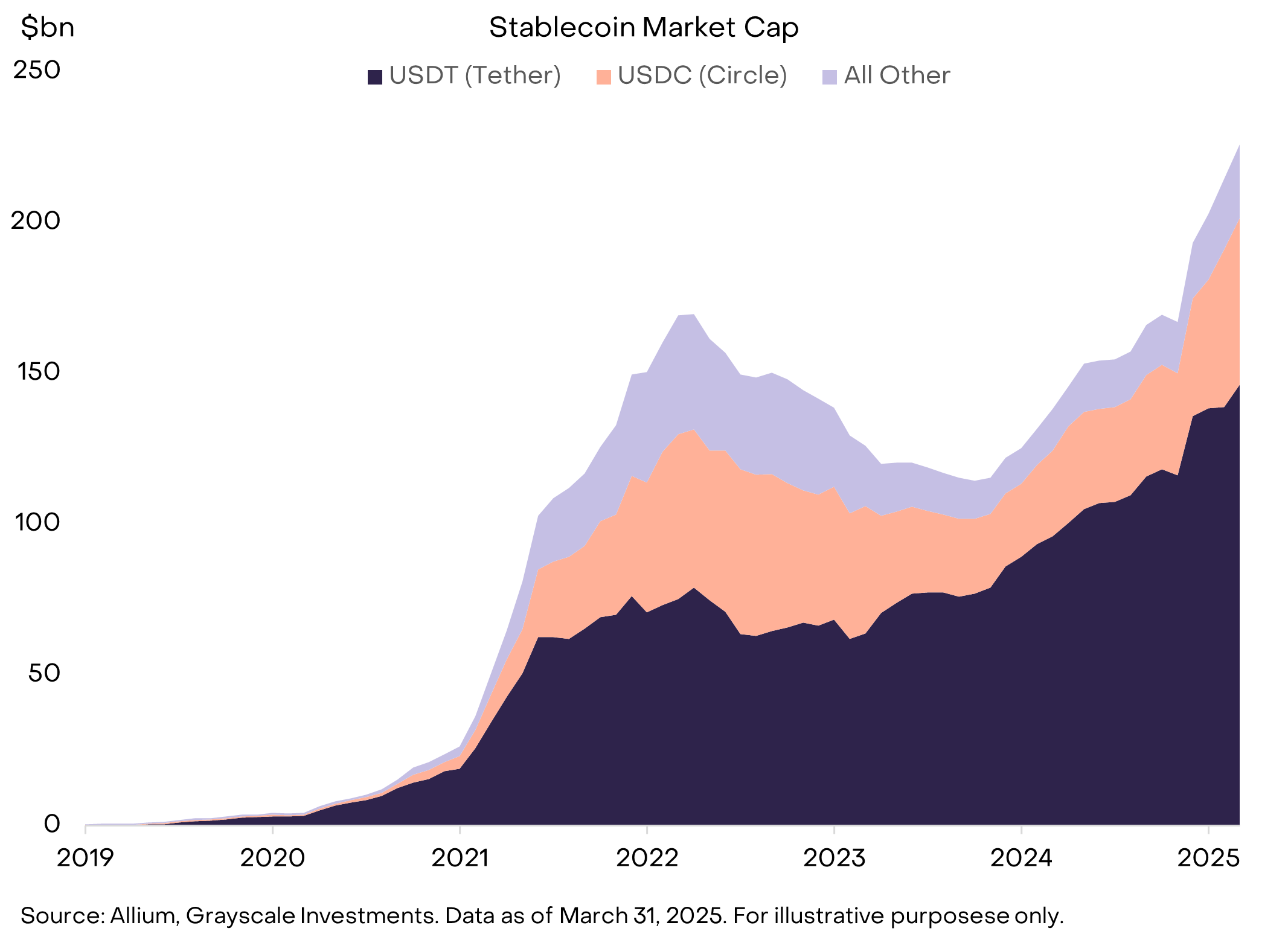

Second, more institutions are getting involved in stablecoins ahead of possible legislation from the U.S. Congress this year (Exhibit 3). For example, according to press reports, both Fidelity and President Trump’s World Liberty Financial plan to launch Dollar-backed stablecoins.[5] Several large fintechs have also made shifts into the stablecoin business. In a deal announced last year that closed in February, payments technology provider Stripe acquired Bridge, a specialist in stablecoin infrastructure.[6]Similarly, PayPal launched its own stablecoin in August 2023 (PYUSD) — which now has a market cap of about $725mn — and press reports suggest that Revolut has plans to launch a stablecoin in the future (aside from stablecoins, last month Revolut extended its crypto trading app to mobile users).[7]

Exhibit 3: Congress may soon take up stablecoin legislation

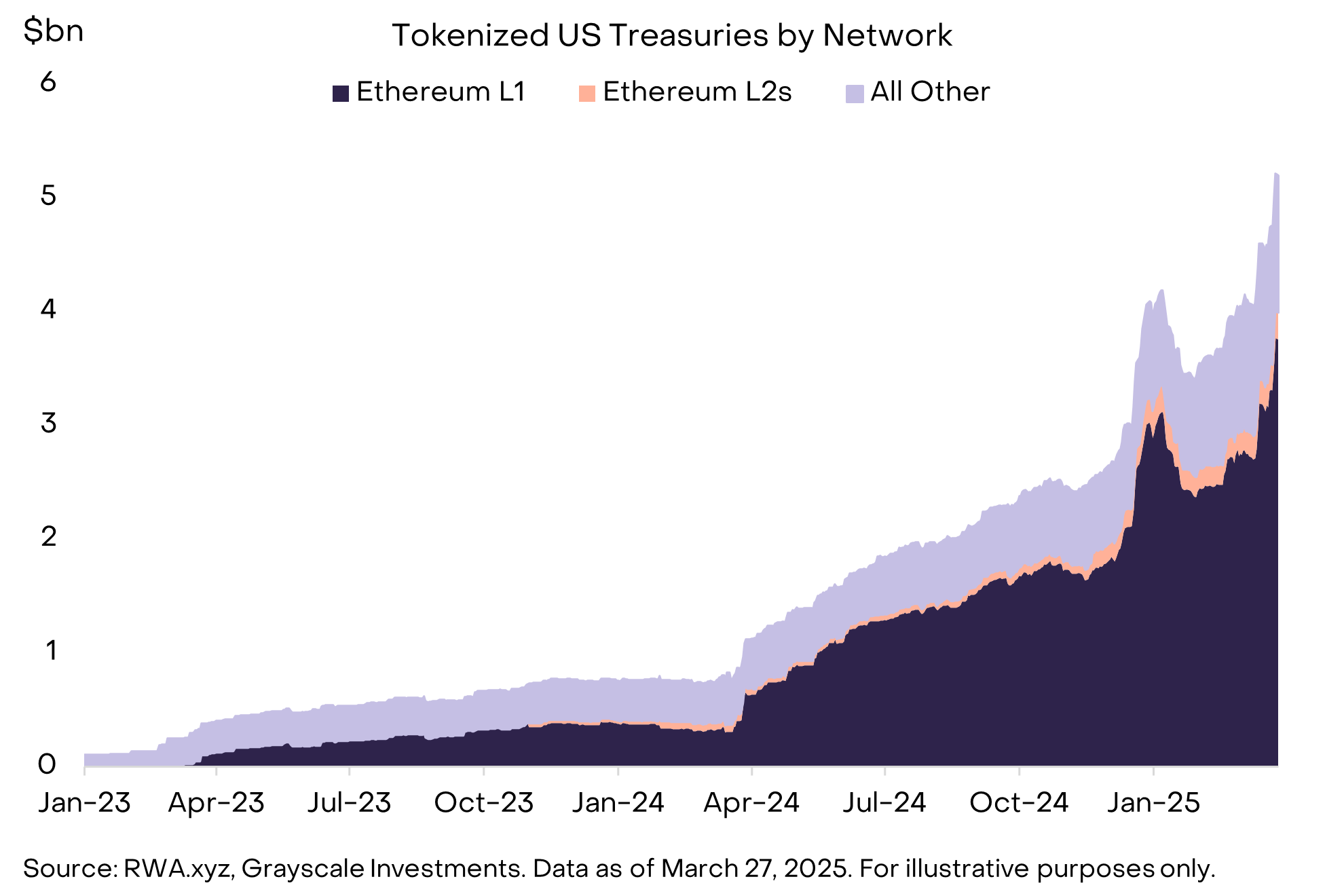

Third, tokenization of real-world assets (RWAs) is heating up (for background, see Public Blockchains and the Tokenization Revolution). According to data platform RWA.xyz, the total amount of tokenized assets (not including stablecoins) reached a record $19.5bn in March.[8] The increase primarily reflected growth in BlackRock’s tokenized Treasury product BUIDL, which reached a market cap of nearly $2bn (Exhibit 4). Growth in tokenized assets may lead to higher demand for “institutional DeFi” (decentralized finance) applications, and recent news showcased investment in related infrastructure. For instance, Coinbase announced the creation of verified pools — essentially a decentralized exchange (DEX) structure with verified identities — and Securitize partnered with Ethena to launch a blockchain providing “compliant access” to DeFi.[9] The Securitize/Ethena project will involve a variety of other industry partners, including Maple Finance, which was recently highlighted in the Grayscale Research Top 20.

Exhibit 4: Record high for tokenized assets

Fourth, more companies are adding Bitcoin to their balance sheet.[10] Strategy (formerly MicroStrategy), which pioneered the approach, purchased another 29k Bitcoin (~$2.4bn) in March 2025 and has accumulated more than 275k Bitcoin (~$23bn) since announcing its current buy program in November. Many Bitcoin miners also now retain Bitcoin on balance sheet (or even purchase Bitcoin in the open market); MARA, the largest mining “hodler,” purchased an additional 715 Bitcoin (~$60mn) during the last month and began a $2bn equity sale to fund future purchases.[11] In late March, video game retailer GameStop said that its board had approved the addition of Bitcoin as a treasury reserve asset.[12] Other recent corporate Bitcoin buyers include video sharing platform Rumble and energy storage company KULR.

Last, but certainly not least, the United States established a Strategic Bitcoin Reserve.[13] In an Executive Order issued on March 6, President Trump created the reserve in part because there is “a strategic advantage to being among the first nations” to treat Bitcoin as a reserve asset. The order mandates the reserve to be capitalized by all Bitcoin currently held by government agencies, that the Bitcoin “shall not be sold,” and that the secretaries of Treasury and Commerce “shall develop strategies for acquiring additional” Bitcoin. Separately, the order also created a “digital asset stockpile,” which will hold (and potentially liquidate) positions in digital assets besides Bitcoin; it also instructed government agencies to conduct a full accounting of any digital assets in possession. Estimates suggest the U.S. government current has claim to 103k Bitcoin ($8.7bn) and around $400mn of other digital assets.[14]

The announcement of the Strategic Bitcoin Reserve initially disappointed some market participants because it did not include immediate new purchases of Bitcoin in the open market. We think this is short-sighted. Treating Bitcoin and public blockchain technology as strategically important could force other nations to reconsider their policies toward the crypto industry — potentially accelerating global adoption. The most important country to watch in this regard is China. Currently, government policy in China bans most crypto activities, including trading and mining, but allows holding of crypto assets. However, policymakers have allowed an expansion of crypto-related activity in Hong Kong under the "one country, two systems" framework. Interestingly, in February, China's Supreme Court and other judicial bodies discussed how to handle crypto in future legal cases — suggesting regulators may be taking a fresh look at the legal treatment of digital assets. If China eases its crypto restrictions, it could significantly boost Bitcoin's global adoption.

Navigating the Macro Risks

Although crypto fundamentals seem to be improving, valuations are down about 30% year to date, based on our market cap-weighted Crypto Sectors index. Crypto is a unique alternative assert class with a relatively low correlation to equity returns, but the market is still subject to broad shifts in the macro outlook and/or investor risk appetite.

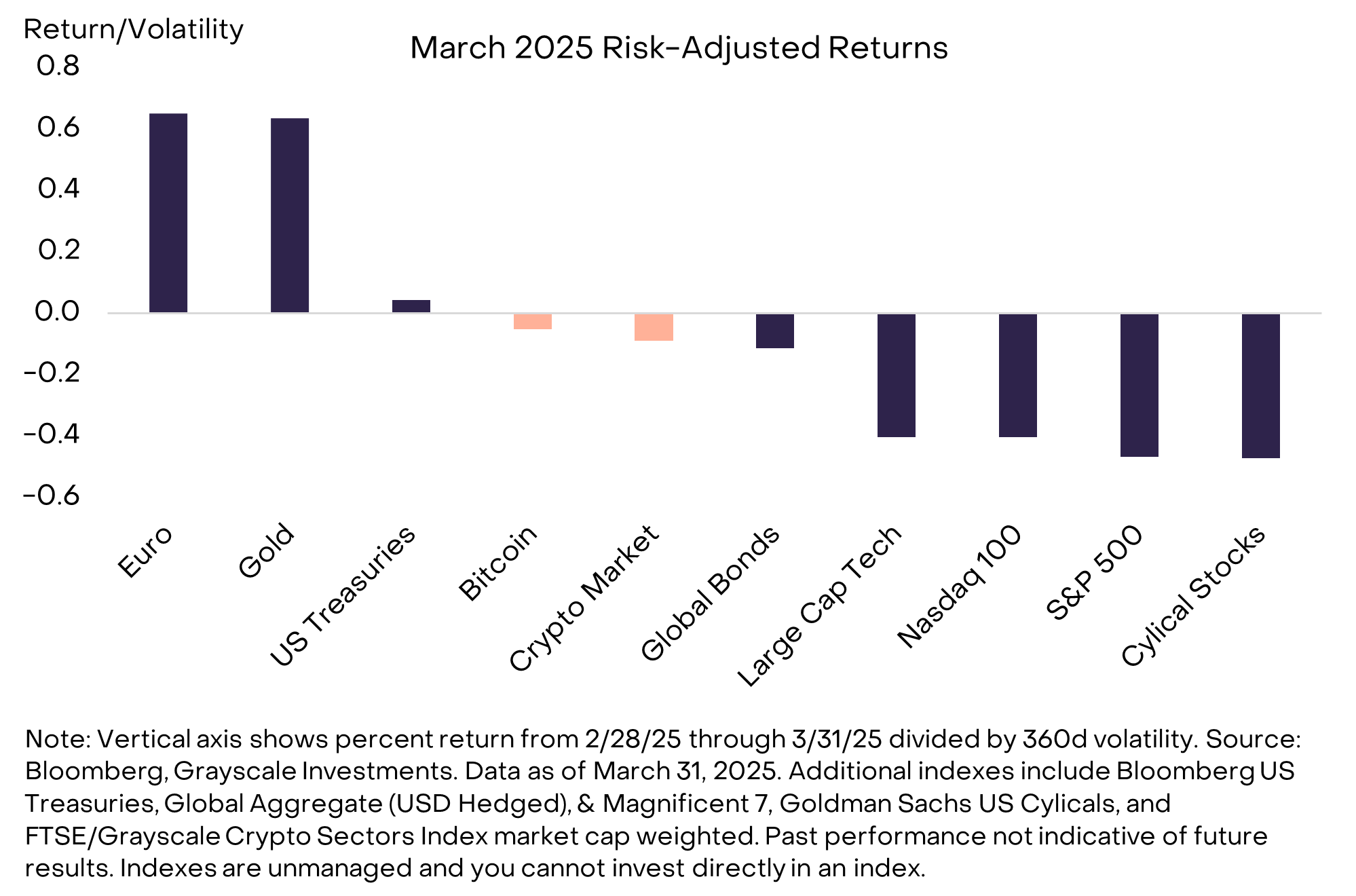

Much of the recent market volatility results from changes in U.S. government policies. Over the coming years, the policy decisions put in place by the Trump administration will have a wide range of effects on the economy, many of which could be positive for productivity growth, domestic employment, and corporate profits. However, the White House has chosen to front-load certain policies — including immigration restrictions, government spending cuts, and tariffs — that may have a negative short-run impact on economic output. As a result, economists have begun marking down their GDP growth forecasts for this year, and public companies have started lowering guidance on earnings. The downgrade to the near-term outlook triggered a significant pullback in global equities and broader derisking, ultimately weighing on Bitcoin and other crypto assets (Exhibit 5).

Exhibit 5: Bitcoin declined with stocks in Q1 2025

There is still high uncertainty about the near-term U.S. policy outlook, and therefore ongoing macro risks for crypto. But markets have already repriced significantly, so the drag to growth from tariffs should be at least partly discounted. For instance, the market cap of “magnificent 7” large-cap tech stocks has declined by more than $3tr since the highs in mid-December (an amount greater than the market cap for the entire crypto asset class).

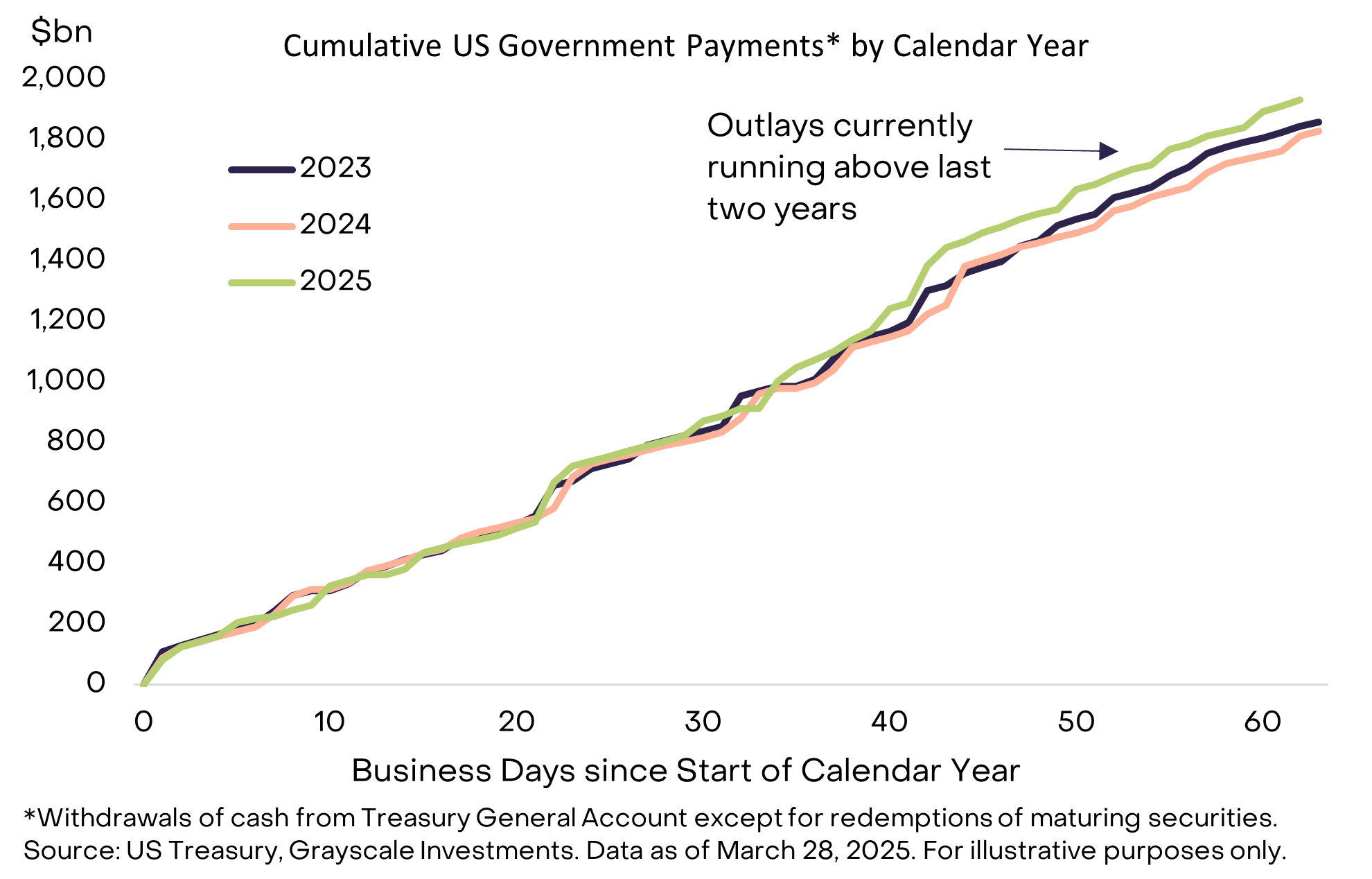

Moreover, the near-term downside risks to growth from cuts by the Department of Government Efficiency (DOGE) may be overstated. The agency claims $130bn in savings (0.4% of GDP), but much of this must be deferred payments and there is no evidence the U.S. Treasury is making fewer payments — in fact, total U.S. government outlays year to date are currently tracking above both 2023 and 2024 (Exhibit 6). Significant cuts to government spending could be incorporated into the tax bill (“budget reconciliation”) currently moving through Congress, but it is unclear what magnitude of cuts will have sufficient support.

Exhibit 6: So far, little evidence of reduced government spending

Grayscale Research therefore continues to see a favorable baseline outlook for crypto markets, reflecting both positive fundamental trends for the digital assets industry itself and a broadly supportive macro markets backdrop. In a recession scenario — caused by a trade war, deep government spending cuts, and/or other drivers — crypto valuations could decline further. But if policy uncertainty declines and the economy continues to hold up, crypto valuations could rebound relatively quickly, given the latest pullback and solid industry fundamentals. For investors who have not previously allocated to crypto, the decline in valuations since the start of 2025 offers a potentially compelling entry point, in our view, for building a longer-term position in the asset class.

[1] For example, in monthly returns over the five years ending March 31, 2025, Bitcoin had a correlation of +0.6 with the S&P 500 and -0.2 with the DXY index. Source: Bloomberg, Grayscale Investments.

[3] Source: Bloomberg, Bloomberg.

[5] Source: Financial Times, Reuters.

[7] Source: Artemis, CoinDesk, The Block. Data as of March 31, 2025.

[8] Source: RWA.xyz. The total is about $10bn excluding Figure.

[9] Source: Coinbase, Securitize.

[10] All statistics in this paragraph come from bitcointreasuries.net.

[13] Source: White House.

[14] Source: Arkham Intelligence, CoinDesk, CoinTelegraph, Grayscale Investments. US government Bitcoin claims calculated by Grayscale Investments as the 198,012 Bitcoin in US government addresses according to Arkham Intelligence, minus the 94,643 Bitcoin owned to Bitfinex. Data as of March 31, 2025.