Grayscale Research Insights: Crypto Sectors in Q2 2025

Research Team

Last Updated: 3/26/2025 | 13 min. read

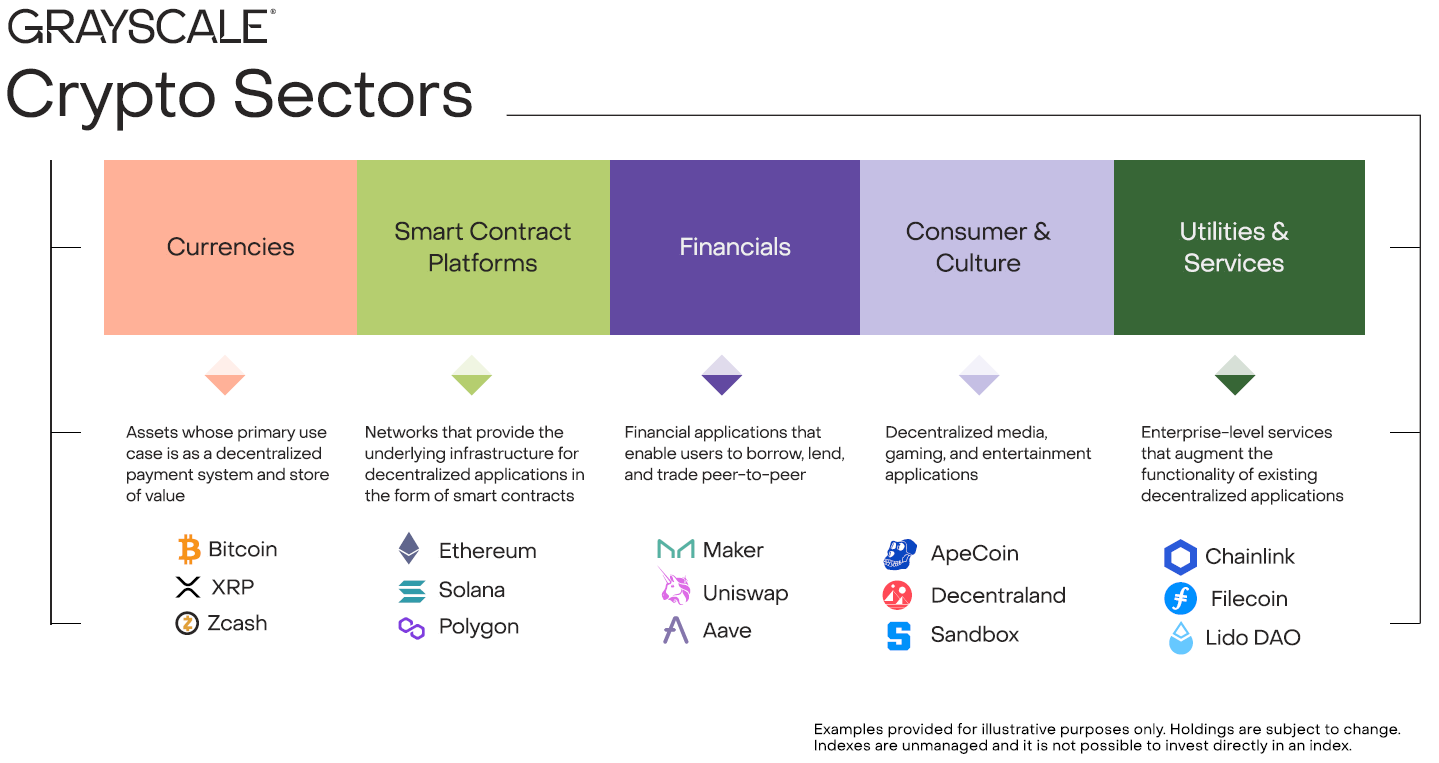

There are now more than 40 million tokens across the digital assets industry (not including NFTs).[2] To keep track of it all, Grayscale Research organizes the marketplace into five distinct Crypto Sectors based on the de facto use of the underlying software (Exhibit 1). Investors can monitor the performance of each market segment through our Crypto Sectors family of indexes, developed in partnership with FTSE/Russell. As of our latest index rebalancing, the Crypto Sectors framework now encompasses 227 distinct assets with an aggregate market capitalization of $2.6 trillion — about 85-90% of estimates of total crypto market cap.[3]

Exhibit 1: Crypto Sectors divides digital assets into five market segments

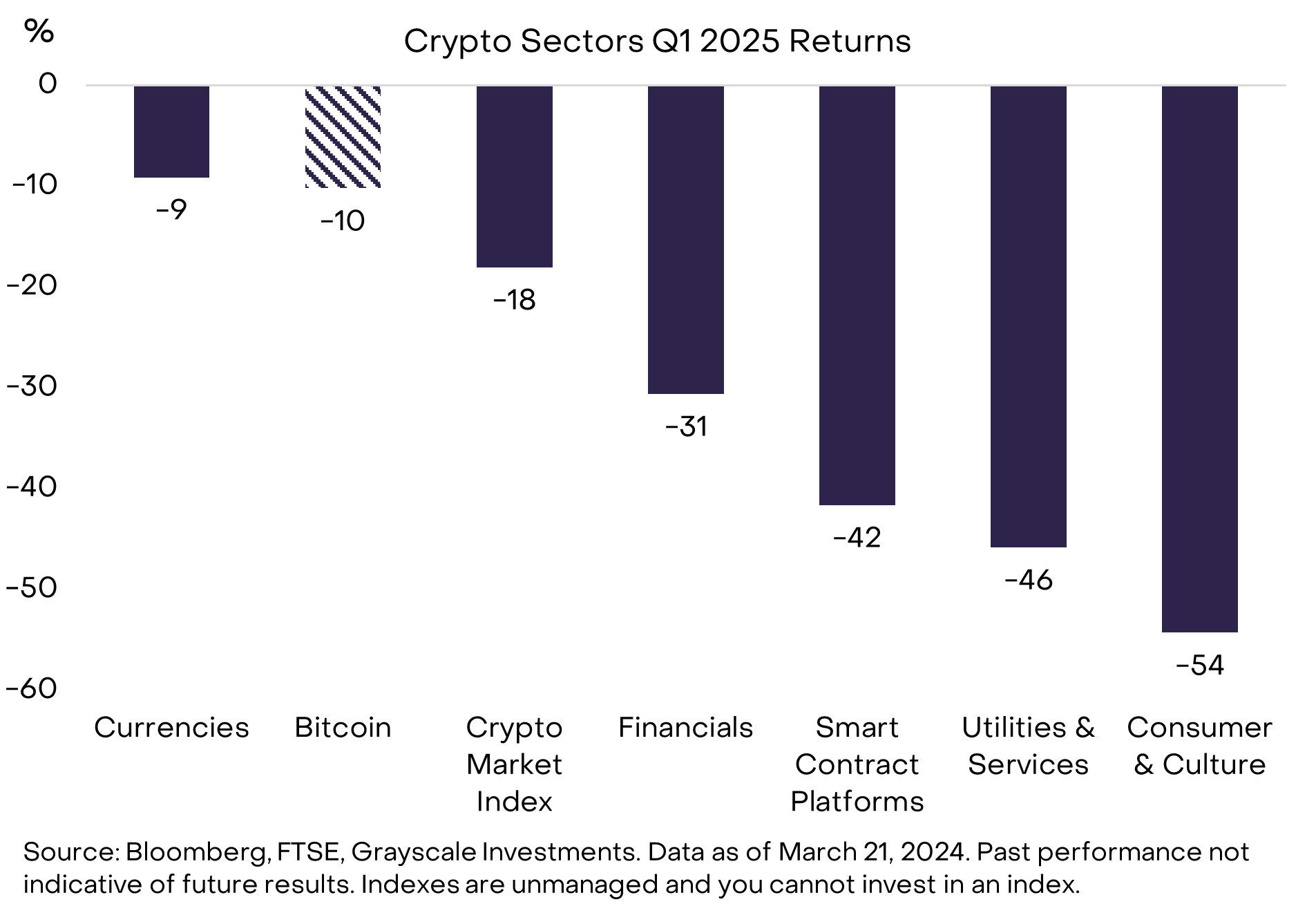

Crypto valuations declined across the board in Q1 2025, alongside technology shares and risky assets in general (Exhibit 2). Our industry-wide market cap-weighted Crypto Sectors price index fell 18% during the quarter (through Friday March 21). Bitcoin and some other components of the Currencies Crypto Sector fell by smaller amounts or increased in price (e.g., XRP). The weakest market segment during the quarter was Consumer & Culture, primarily due to declines in the price of Dogecoin and other memecoins.

Exhibit 2: Crypto valuations declined in Q1 2025

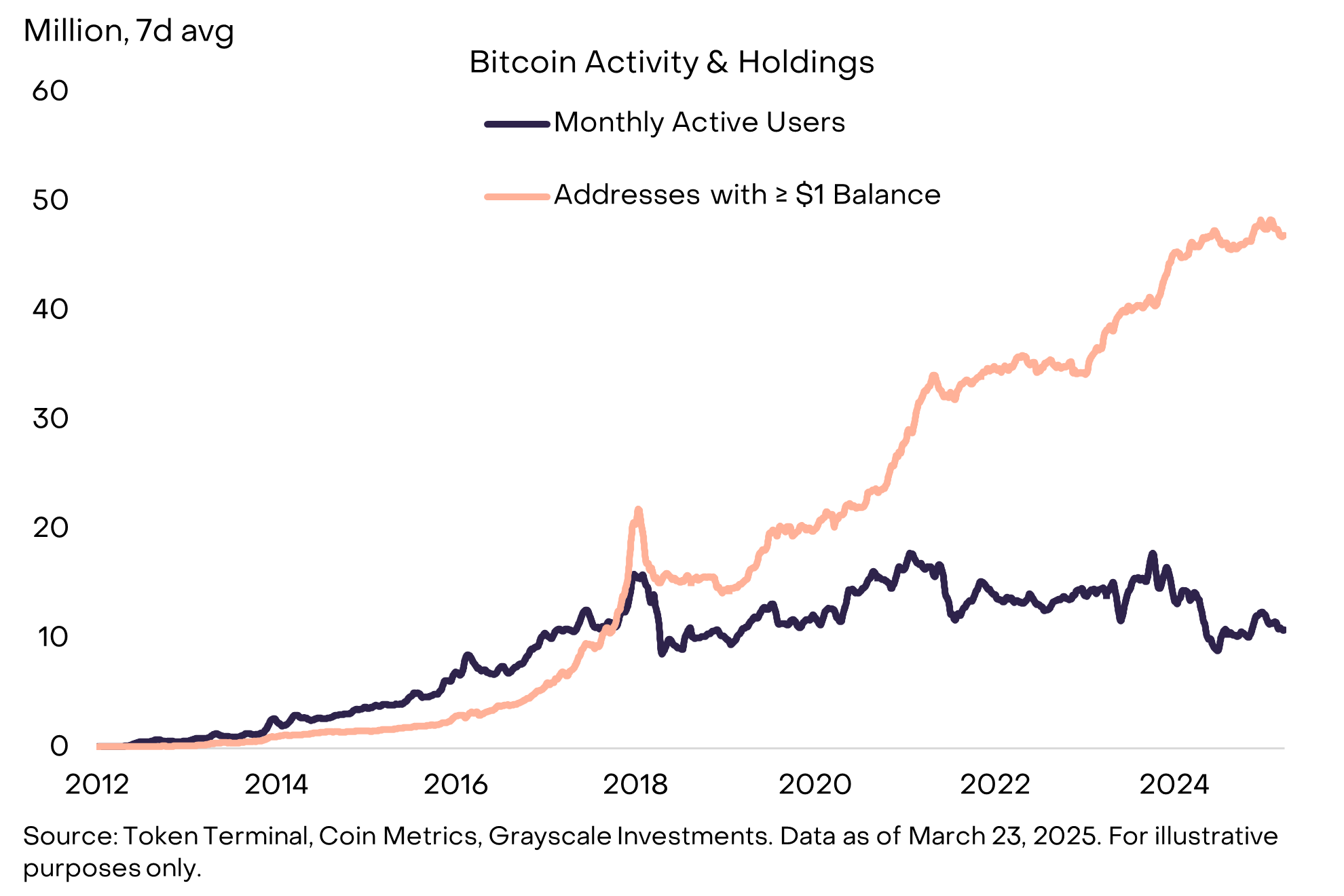

Measures of Bitcoin network activity were generally healthy in Q1 (see Exhibit 6 below for a summary of Crypto Sectors fundamental indicators). For example, the number of addresses with a balance greater than or equal to $1 — a crude measure of “hodler” demand — reached a new high of 48 million. In contrast, monthly active on-chain users were about unchanged from the prior quarter at 11 million. The growing difference between these two indicators suggests that recent demand for Bitcoin has likely come from users interested in its function as a “store of value” rather than a “medium of exchange” (Exhibit 3). Bitcoin’s hash rate increased to nearly 800 exahash per second (EH/s) in Q1, meaning the network of 5-6 million Bitcoin mining rigs around the world was attempting to solve the Proof of Work algorithm roughly 800 quintillion times every second (for more background, see our report The Power of Bitcoin Mining).

Exhibit 3: Steady growth in number of Bitcoin “hodlers”

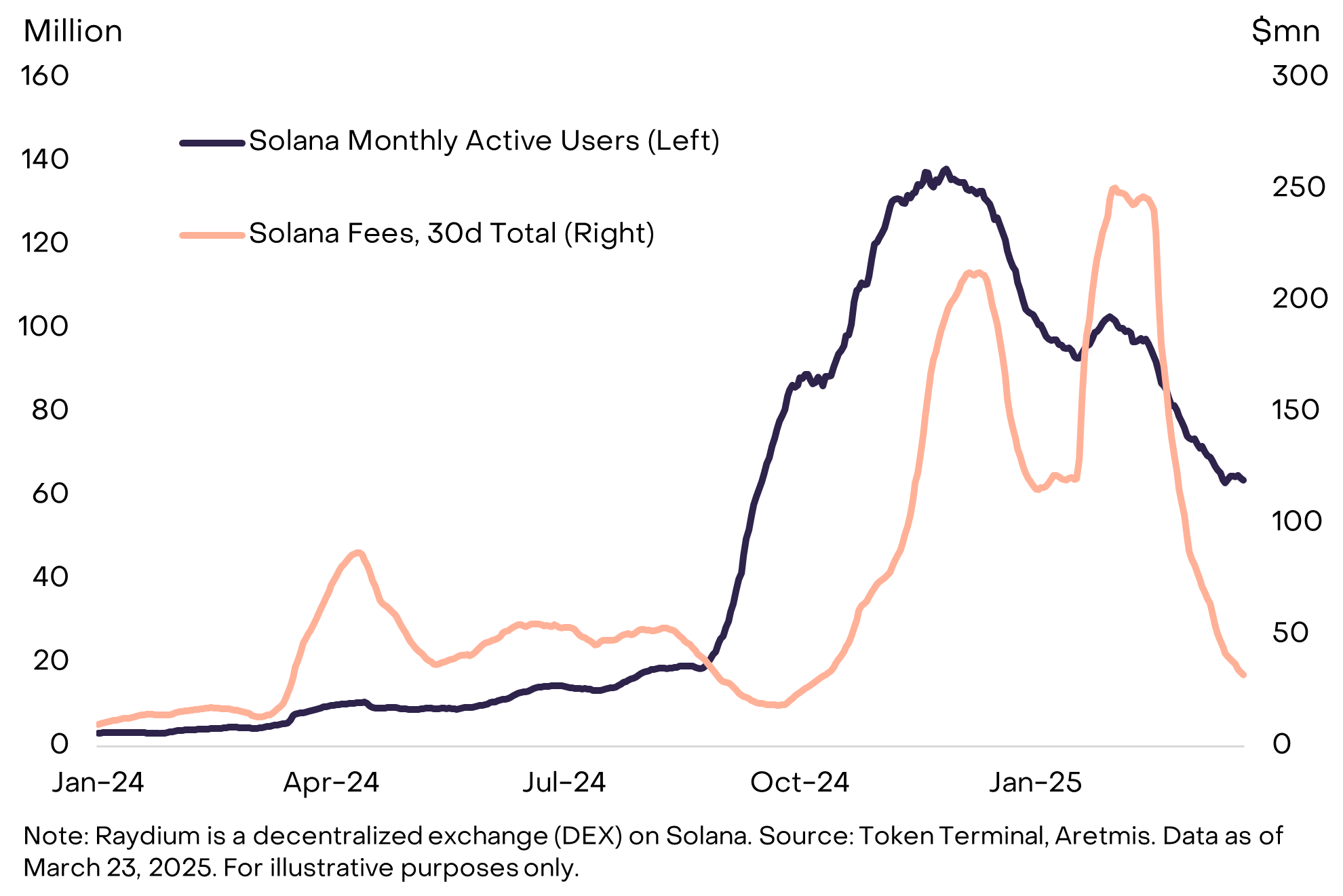

Fundamental indicators for the Smart Contract Platforms Crypto Sector generally declined in early 2025, largely due to a pullback in memecoin trading activity on the Solana blockchain. Although memecoins do not claim to offer real-world utility — and can be associated with especially high risks for investors — interest in memecoin trading may have introduced new users to the Solana ecosystem. According to data from Token Terminal, monthly active Solana users reached 140 million in late Q4 and averaged nearly 90 million in Q1 (Exhibit 4). Even with the slowdown in memecoin trading, Solana generated about $390 million in fees in Q1, or just under half of estimated total fees for smart contract platforms.[4]

Exhibit 4: Solana monthly active users reached ~140 million at the peak

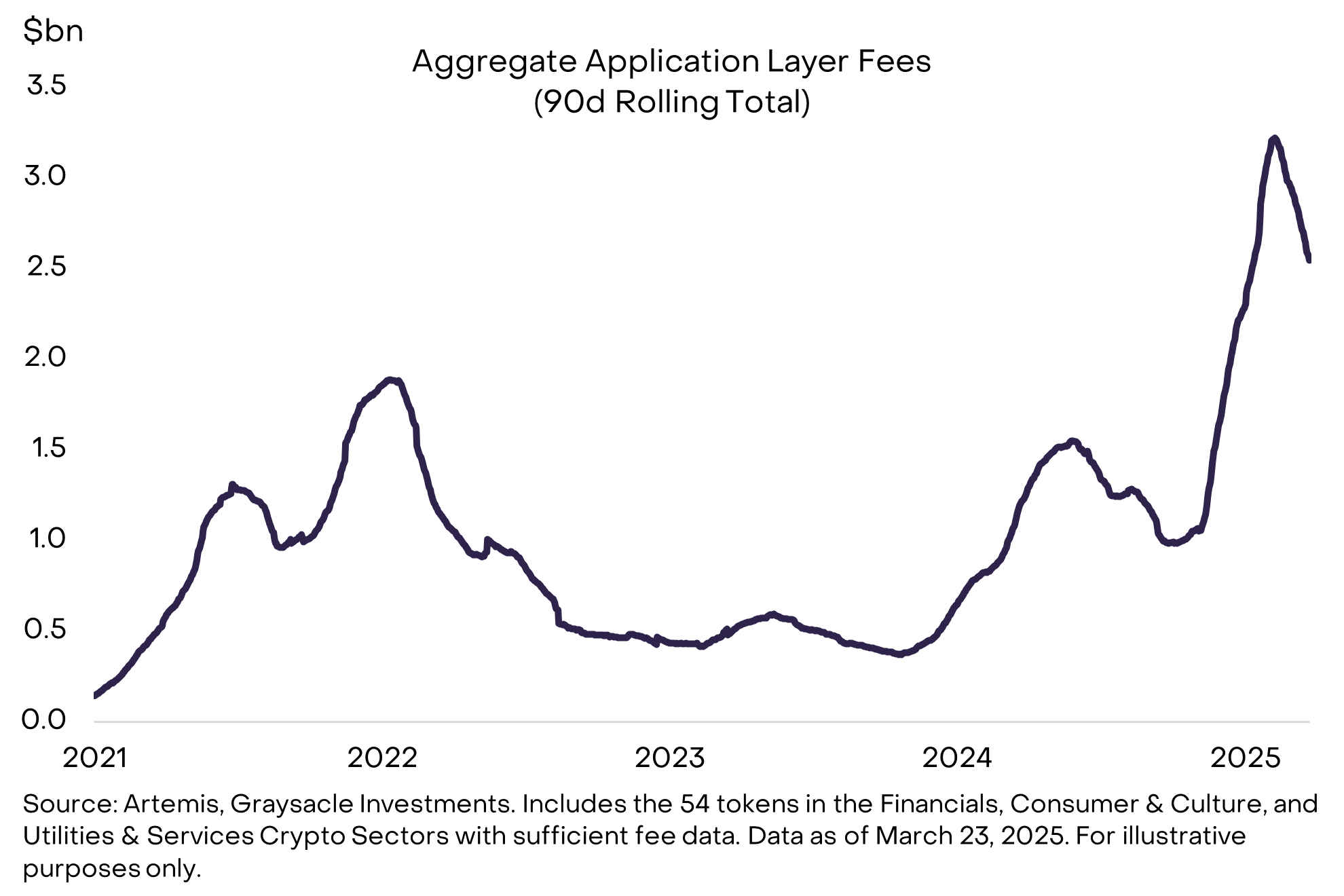

The Grayscale Crypto Sectors framework includes three categories for application-related crypto assets: Financials, Consumer & Culture, and Utilities & Services. These market segments include all the components of on-chain economic activity, including user-facing applications, related application infrastructure (e.g., oracles and bridges), and special-purpose blockchains. The category is therefore highly diverse, and we believe the assets are best evaluated against narrow peer groups focused on the specific use case. That being said, for the subset of assets in our three application layer Crypto Sectors categories,[5] we estimate that fees totaled about $2.6bn, implying an increase of 99% from the first quarter of 2024 (Exhibit 5).

Exhibit 5: Blockchain applications generating >$2bn in quarterly fees

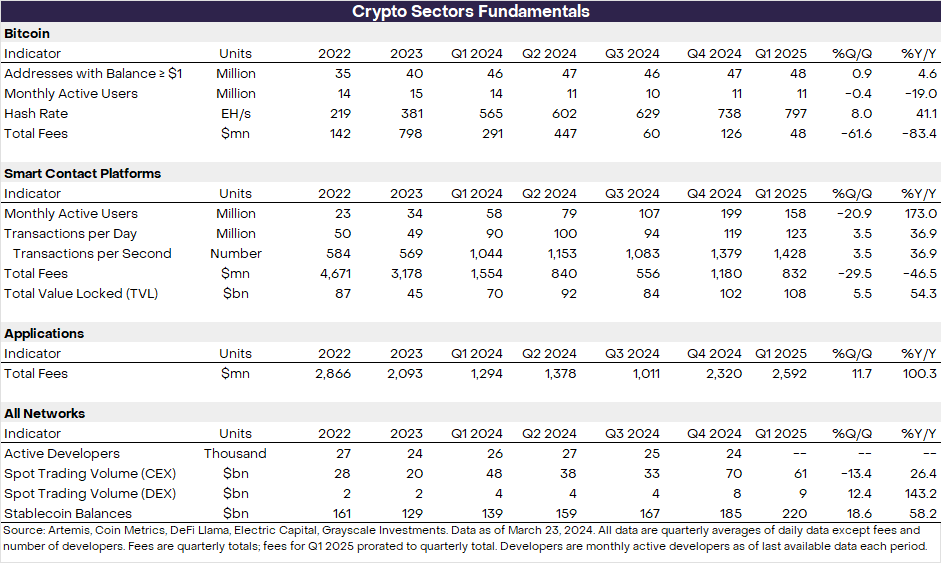

Exhibit 6 provides a few key fundamental statistics for segments of the digital assets marketplace. In general, the metrics show solid growth from a year earlier, but more mixed changes over the last quarter.

Exhibit 6: Blockchain applications generating >$2bn in quarterly fees

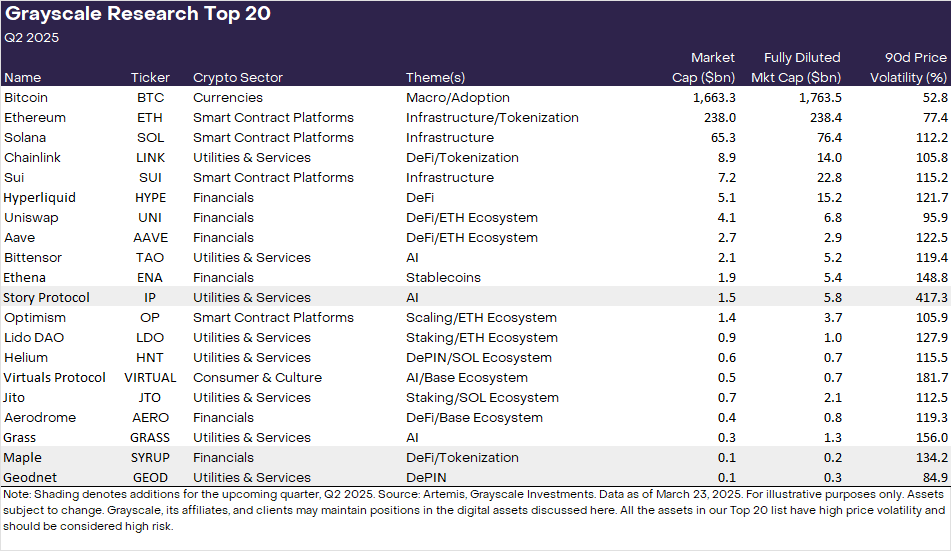

The Grayscale Research Top 20

Each quarter the Grayscale Research team analyzes hundreds of digital assets to inform the rebalancing process for the FTSE/Grayscale Crypto Sectors family of indexes. Following this process, Grayscale Research produces a Top 20 list of assets within the Crypto Sectors universe. The Top 20 represents a diversified set of assets across Crypto Sectors that, in our view, have high potential over the coming quarter (Exhibit 7). Our approach incorporates a range of factors, including network growth/adoption, upcoming catalysts, sustainability of fundamentals, token valuation, token supply inflation, and potential tail risks.

Over the past quarter Grayscale Research has been encouraged by examples of emerging assets on the blockchain application layer (as opposed to the infrastructure layer). This quarter we are emphasizing tokens that reflect real-world, non-speculative applications of blockchain technology that fall into one of three categories: tokenization of RWAs (real-world assets), DePIN (decentralized physical infrastructure), and IP (intellectual property).

We believe that progress with these emerging non-speculative use cases such as the three listed above reflects positive signs of crypto industry maturation.

Exhibit 7: Our updated Top 20 now features SYRUP, GEOD, and IP

In addition to the new themes mentioned above, we continue to be excited about themes from previous quarters such as Ethereum scaling solutions, the intersection of blockchain and AI development, and DeFi and staking solutions. Each of these themes is represented by the inclusion of protocols that return to the top 20, such as Optimism, Bittensor, and Lido DAO, respectively.

This quarter we have rotated the following out of the Top 20: Akash, Arweave, and Jupiter. Grayscale Research continues to see value in each of these projects, and they remain important elements of the crypto ecosystem. However, we believe the revised Top 20 list may offer more compelling risk-adjusted returns for the coming quarter.

Investing in the crypto asset class involves risks, some of which are unique to the crypto asset class, including smart contract vulnerabilities and regulatory uncertainty. Moreover, all the assets in our Top 20 have high volatility and should be considered high risk and are therefore not suitable for all investors. In light of the risks to the asset class, any investment in digital assets should therefore be considered in the context of a portfolio and with consideration of an investor’s financial goals.

Index Definition: The FTSE/Grayscale Crypto Sectors (CSMI) measures the price return of digital assets listed on major global exchanges. The FTSE Grayscale Smart Contract Platforms Crypto Sector Index was developed to measure the performance of crypto assets that serve as the baseline platforms, upon which self-executing contracts are developed and deployed. The FTSE Grayscale Utilities and Services Crypto Sector Index was developed to measure the performance of crypto assets that aim to deliver practical and enterprise-level applications and functionalities. The FTSE Grayscale Consumer and Culture Crypto Sector Index was developed to measure the performance of crypto assets that support consumption-centric activities across a variety of goods and services. The FTSE Grayscale Currencies Crypto Sector Index was developed to measure the performance of crypto assets that serve at least one of three fundamental roles: store of value, medium of exchange, and unit of account. The FTSE Grayscale Financials Crypto Sector Index was developed to measure the performance of crypto assets that seek to deliver financial transactions and services.

[1] Artemis, Grayscale Investments, data from Jan 1 through March 25, 2025.

[2] Source: Dune Analytics.

[3] Source: Artemis, Grayscale Investments. Data as of March 24, 2025. Total crypto market cap excludes stablecoins. The FTSE/Grayscale Crypto Sectors family of indexes were rebalanced on March 21, 2025.

[4] Source: Artemis, Grayscale Investments. Data as of March 23, 2025. Fees through March 23 prorated for quarterly total.

[5] Includes 54 constituent assets as of March 23, 2025.

[6]Artemis, data as of March 25, 2025