April 2025: Still Point in a Turning World

Research Team

Last Updated: 5/1/2025 | 11 min. read

In August 1971, President Richard Nixon announced 10% across-the-board tariffs on U.S. imports and ended the convertibility of Dollars into gold. Allies were not consulted in advance, even though the actions ended the multilateral Bretton Woods exchange rate system in place since World War II. The so-called “Nixon Shock” was followed by extensive negotiations over the next four months, culminating in the Smithsonian Agreement in December 1971, in which G10 nations agreed to revalue their currencies versus the Dollar in exchange for tariff relief. While the tariffs were ultimately short-lived, the events changed global trade flows and had long-lasting implications for financial markets (Exhibit 1).

Exhibit 1: U.S. Dollar slid ~30% in years following the Nixon Shock

There are many differences between that period and today, and it will likely take a few months before we know where tariff rates will stabilize — Treasury Secretary Bessent said that the third quarter was a “reasonable estimate” for when markets will have clarity on tariffs.[1] But regardless of how the negotiations play out, like the Nixon Shock in 1971, we expect that President Trump’s push to reshape global trade will have significant implications for the economy and financial markets over the coming years. Investors will need to consider the implications for their portfolios and may need to seek out alternative sources of return and diversification.

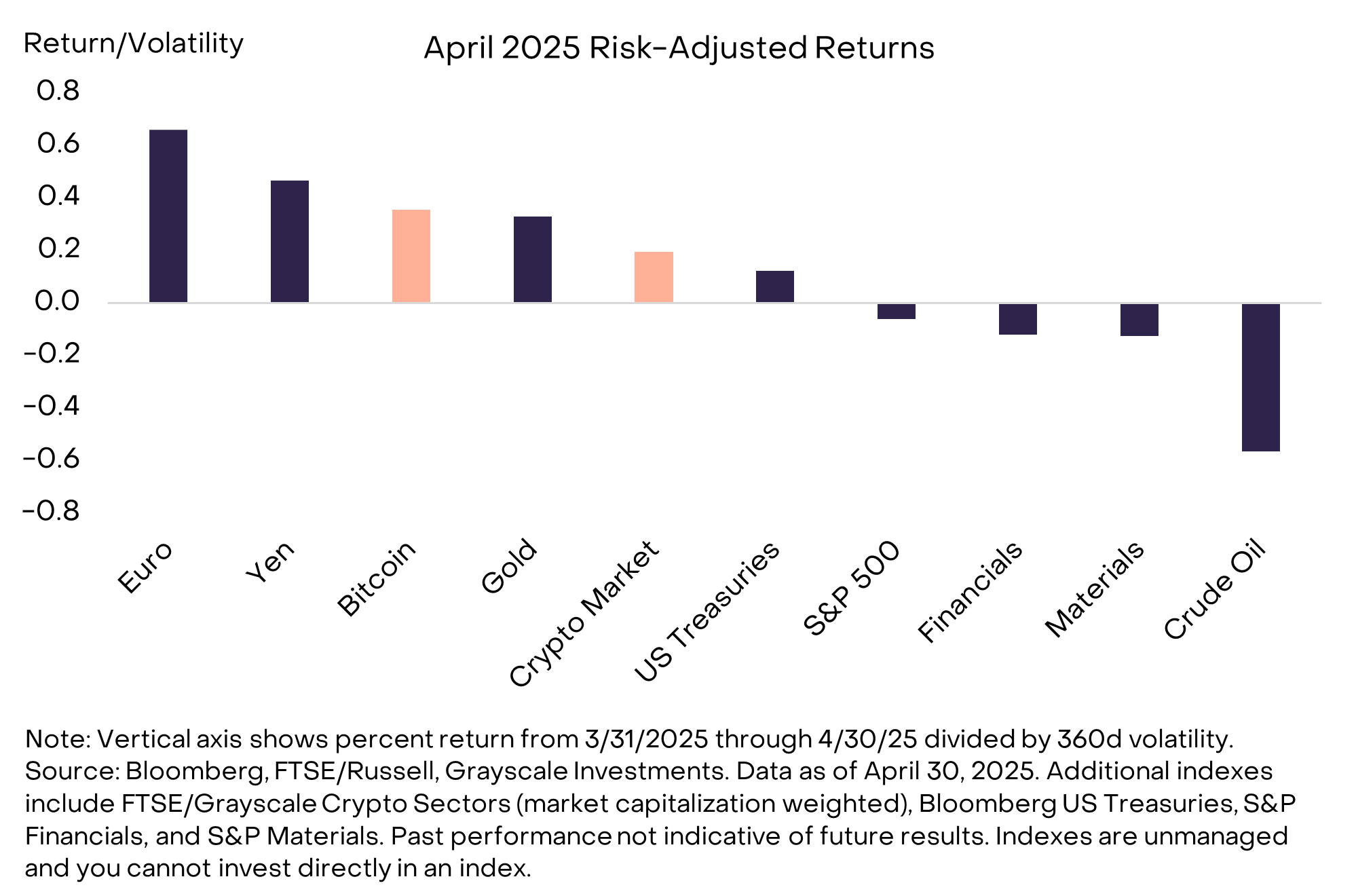

Encouragingly, market performance during April 2025 suggests that Bitcoin and other digital assets may be part of the solution (Exhibit 2). In a volatile month for traditional assets — in which the VIX briefly exceeded 50% — Bitcoin’s price appreciated 15% and our market-cap weighted Crypto Sectors index gained 11%. U.S. equities declined 1% on net, with weakness led by cyclical market segments. Gold and certain foreign currencies had gains comparable to Bitcoin on a risk-adjusted basis (i.e., accounting for each asset’s volatility).

Exhibit 2: Bitcoin appreciated in April alongside other “stores of value”

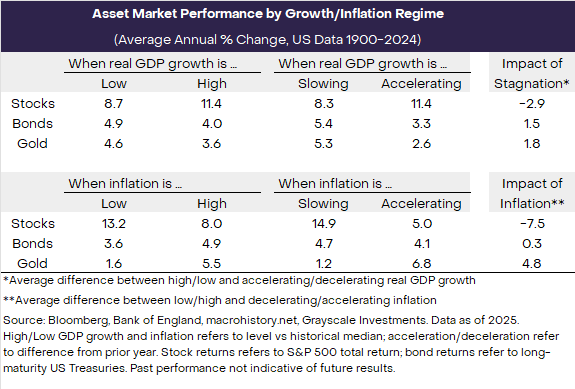

Tariffs and trade conflicts have no direct impact on Bitcoin and may increase adoption over the medium term. First, stagflation tends to be harmful for traditional assets like stocks and positive for scarce commodities like gold (Exhibit 3). Bitcoin was not around for past stagflations but can also be considered a scarce digital commodity and is increasingly viewed as a modern store of value. Second, trade tensions may put pressure on reserve demand for the U.S. Dollar, opening space for competing assets, including other fiat currencies, gold, and Bitcoin (for more detail, see Market Byte: Tariffs, Stagflation, and Bitcoin). For these reasons, events over the last month have increased our confidence that portfolio demand for Bitcoin will continue to grow over the coming year.

Exhibit 3: Stagflation should be considered negative for equity markets

Bitcoin purchases by public companies have been one consistent source of demand. Strategy (formerly MicroStrategy), which pioneered corporate Bitcoin investing, purchased another 25k Bitcoin (~$2.4bn) during April. Strategy now holds roughly 3% of the circulating supply valued at more than $50bn.[2] Separately, a consortium including Tether, Bitfinex, Softbank, and Cantor Fitzgerald announced the creation of Twenty One Capital, a new company initially capitalized with 42,000 Bitcoin.[3] At that size Twenty One Capital would have the third-largest Bitcoin portfolio among public companies, after Strategy and Bitcoin miner MARA.[4] The company will go public through a SPAC (special-purpose acquisition company), which currently trades as Cantor Equity Partners (ticker: CEP).

Although tariffs and trade conflict dominated market attention, institutional investment in the crypto industry continued at a healthy pace, supported by increasing regulatory clarity (for more details, see March 2025: Institutional Chain Reaction). There are now two distinct trends: (1) traditional financial services firms investing in crypto, and (2) crypto-native firms starting to offer traditional financial services. Examples from the last month include reporting that Dutch bank ING is working on a stablecoin, moves by Mastercard to bring stablecoins into its payments network, an announcement from crypto exchange Kraken that it will offer equity and ETF trading, news that BitGo and others are working to get U.S. bank licenses, and the introduction of a new payments platform by stablecoin issuer Circle.[5]

In regulatory news, the Federal Reserve said that it had withdrawn earlier guidance about commercial banks’ crypto- and stablecoin-related activities. Previously the Fed had required banks to give advance notice before undertaking any crypto activities; under the updated guidance the Fed will consider banks’ crypto activity as part of its normal supervisory process. Separately, at an event in mid-April, Fed Chair Powell said about the crypto industry: “I think that the climate is changing, and that you are moving into more mainstreaming of that whole sector.” Powell added that he was encouraged by progress on stablecoin legislation in Congress.[6] Although House and Senate negotiators need to iron out some differences, passing stablecoin legislation over the next month still appears possible.[7]

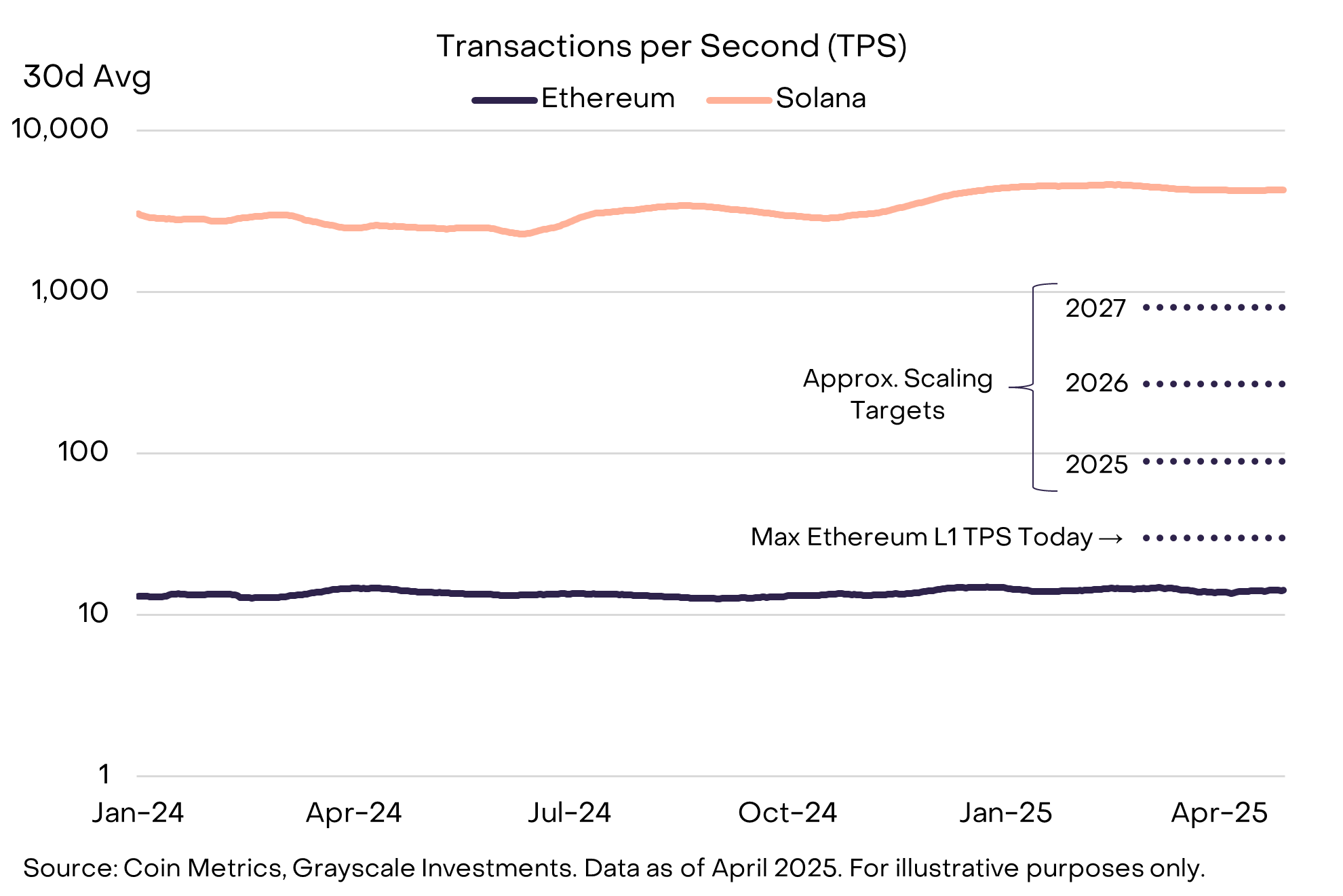

From a technical standpoint, the most important news from the past month was arguably the shift in development priorities by the Ethereum Foundation (EF). There are multiple elements to the changes, but from the standpoint of investing in the Ether (ETH) token, the key change, in our view, was the renewed focus on scaling the Ethereum Layer 1 (i.e., increasing the transaction throughput of the Ethereum mainnet itself). Based on EF comments on social media and elsewhere, the rough expectation seems to be a 3x increase in Layer 1 transactions per second (TPS) each year for several years, with a long-run target of 10,000 TPS (Exhibit 4). Increasing Layer 1 TPS while maintaining a degree of pricing power is the best way to increase transaction fees, reduce token supply, and support the token’s price (for more detail, see Ethereum: The OG Smart Contract Blockchain).

Exhibit 4: Ethereum will refocus on scaling the Layer 1

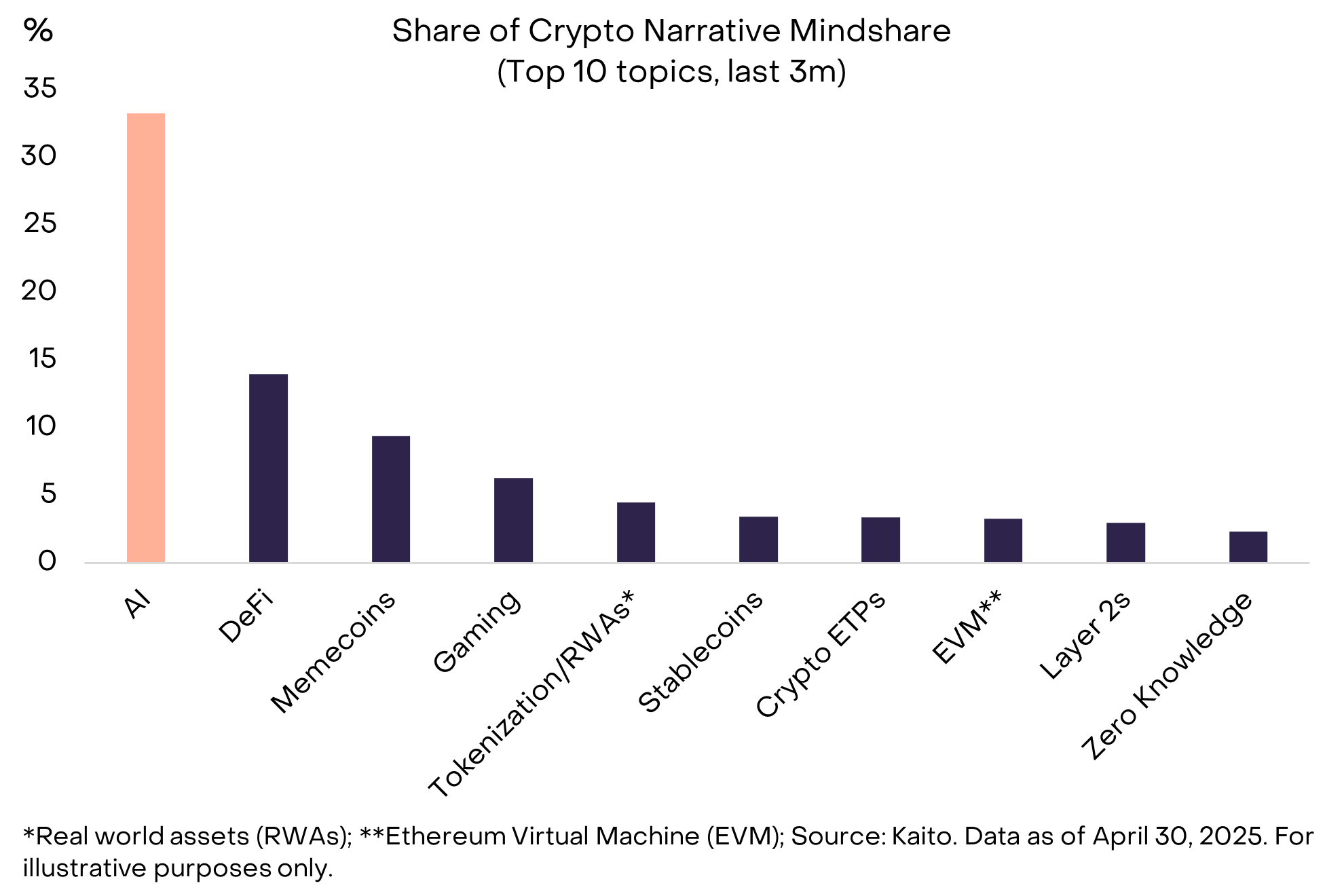

Beyond the large-cap assets, many crypto investors remain focused on blockchain-based artificial intelligence (AI) or decentralized AI (deAI). For example, according to data provider Kaito, AI-related projects accounted for about one-third of crypto industry “mindshare” (social media attention) over the last three months (Exhibit 5). The Bittensor ecosystem in particular has been expanding, driving outperformance of its TAO token. Bittensor now has over 90 active subnets, and subnet tokens have an aggregate circulating market capitalization of $580 million.[8] Other notable crypto/AI developments in April included the first successful decentralized training of a 32bn parameter model by Prime Intellect (a collaboration between Flock.io and Alibaba Cloud), and Nous Research raising $50mm in fundraising led by Paradigm to support decentralized model training on Solana.[9]

Exhibit 5: Beyond macro, decentralized AI remains the biggest story in crypto

The crypto asset class includes a wide range of projects with many different use cases. However, they all share the vision of borderless finance and decentralization. Investors already appreciate these attributes of Bitcoin, which is likely why it performed well during a turbulent month for traditional assets. However, many other crypto assets share these features to a degree and may also be partly immune to tariffs and trade conflict. In our view, persistent uncertainty about government policy, the risk of stagflation, and potentially sustained weakness in the U.S. Dollar will lead investors to seek out alternative sources of return and diversification. We expect the resulting shift in capital flows to continue to benefit Bitcoin and to increasingly support the broader crypto ecosystem.

[2] Source: Bitcointreasuries.net, Coin Metrics, Grayscale Investments. Data as of April 30, 2025.

[3] Source: Cantor Fitzgerald, Financial Times.

[4] Source: bitcointreasuries.net.

[5] Source: CoinDesk, The Block, Kraken, WSJ, Bloomberg.

[9] Source: Prime Intellect, Coinstats, Cointelegraph.