Blockchains secure themselves in one of two ways: Proof of Work (PoW) and Proof of Stake (PoS). PoW relies on energy and machines, while PoS relies on staking and voting. Bitcoin, the largest crypto asset by market capitalization, utilizes PoW. The majority of other well-known blockchains utilize PoS, including Ethereum, Solana, Avalanche, Cardano, and others. Both processes serve as a consensus mechanism to verify and validate transactions on their respective blockchains.

The PoS consensus mechanism relies on so-called validators, who are selected based on the number of tokens they have staked as collateral. In other words, by demonstrating “skin in the game”—putting their token capital at risk—validators show their commitment to the network. By contrast, in a PoW mechanism, miners are selected based on the amount of computing power they bring to the task. Bitcoin consensus, based on PoW, consumes a significant amount of electricity, whereas PoS-based blockchains do not.

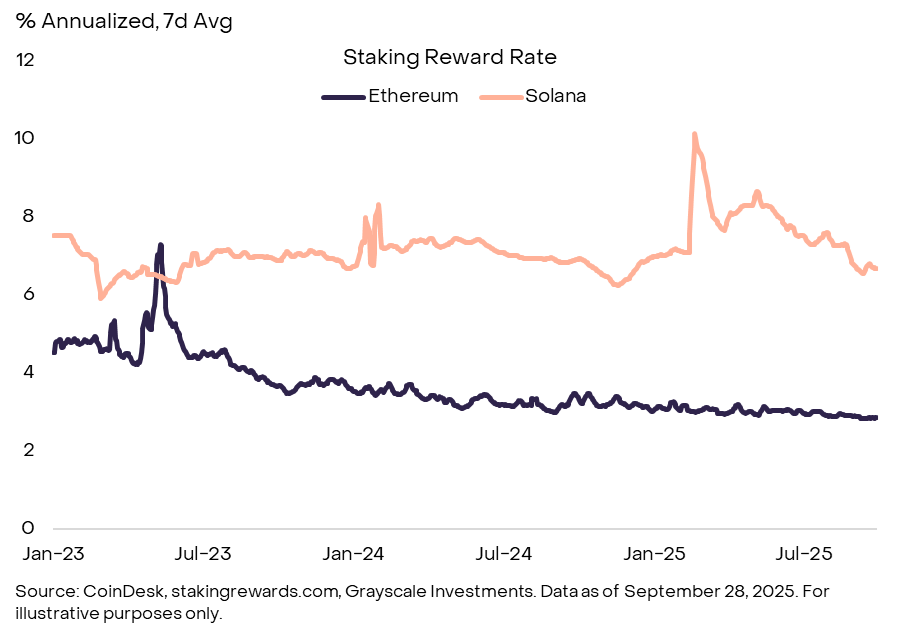

On Ethereum, staking rewards consist of newly-minted Ether (ETH) tokens and transaction fees. In other words, instead of a simple buy-and-hold strategy, owners of ETH who engage in staking are able to generate income from their assets by earning protocol-native rewards. Ethereum stakers currently earn an average reward rate of approximately 3%, depending on network conditions.[1]

Proof of Work vs. Proof of Stake

Proof of Work secures blockchains with electricity and specialized hardware. Miners compete to add blocks and earn rewards through issuance and fees. Bitcoin represents the overwhelming share of PoW assets—some 97%—and about 63% of total crypto market capitalization.[2]

Proof of Stake helps secure blockchains by requiring validators to post or “lock” tokens as collateral. Validators propose and validate blocks and can be rewarded with issuance and fees. In other words, staking is central to the network’s economics and security.

Stakers who perform their duties correctly are rewarded with additional tokens, while those who act against the interest of the chain can see their stake “slashed”—that is, penalized and reduced.[3]

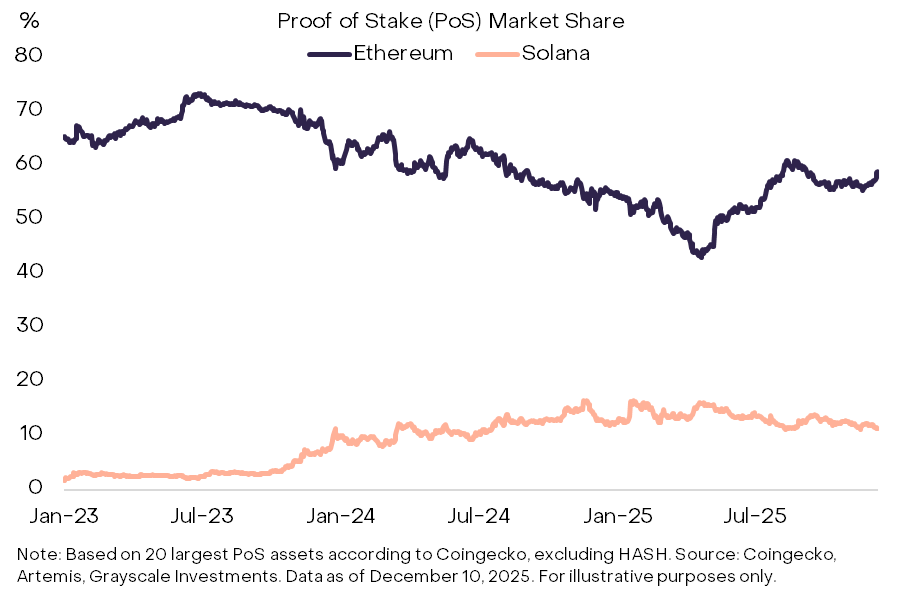

Ethereum switched from PoW to PoS in 2022, and the result was a reduction in energy use of over 99% (for more background see From Miners to Stakers: How Staking Secures the Ethereum Blockchain). Ethereum and Solana are the largest blockchains utilizing PoS today, accounting for roughly 57% and 16% of overall PoS market value, respectively (Exhibit 1). Other notable PoS networks with meaningful market share include Cardano (3%), Hyperliquid (1%), Avalanche (1%), and Sui (1%).[4]

Exhibit 1: Ethereum is largest proof of stake blockchain by market capitalization

Why staking matters

Staking is more than a way to earn rewards—it is the foundation of security and economic design in modern blockchains. When participants stake, they commit capital that protects the network, while earning variable returns linked to network activity.

In the broader digital asset economy, staking functions as infrastructure:

It secures the system without relying on centralized intermediaries.

It generates rewards. Unlike contractual yield from bonds or other fixed income instruments, staking rewards are protocol-driven, variable, and contingent on network factors such as validator performance, token inflation schedules, and governance decisions. These rewards serve as incentives for validators to secure the network and promote its ongoing usage.

It drives competition among service providers and protocols, shaping market structure.

It aligns incentives between token holders, validators, and users, keeping the system balanced.

As digital assets mature, staking will stand alongside payment rails and clearing systems as one of the essential pillars of financial infrastructure. Institutional interest in crypto investments may rise alongside the increased prevalence of staking. Institutions value income, and the ability to add staking rewards to the potential return on crypto investments should boost liquidity and on-chain participation.

Token utility

Native blockchain tokens serve three essential purposes:

Network security: Staked tokens serve as collateral, ensuring validators act honestly and the blockchain remains secure.

Medium of exchange: Tokens are used to pay transaction or “gas” fees, enabling activity on the network.

Investment exposure: Beyond potential price appreciation of the asset itself, token holders can earn staking rewards

Who participates and how

The staking ecosystem is made up of a variety of players, which fall into three main groups:

Validators: Run the technical infrastructure and earn rewards for keeping the blockchain secure.

Delegators: On many networks, token holders can delegate their tokens to validators and share in the rewards without running infrastructure themselves.[5]

Service providers: Custodians, staking-as-a-service firms, liquid staking protocols, and exchanges that make staking more accessible to institutions and individuals.

There are several ways to participate in staking, varying in technical difficulty and risk:

Solo staking: Provides maximum control and contribution to decentralization but requires technical expertise and a large minimum stake.

Non-custodial staking: In non-custodial staking, the investor retains control of their private keys and assets in their own wallet, delegating only the staking function to a validator. The investor is protected from third-party security concerns but is responsible for more technical details than custodial staking, below.

Custodial staking: In custodial staking, investors give their crypto to a third-party service (e.g., an exchange), that stakes on their behalf. This is simpler than both solo and non-custodial staking but introduces reliance on both the validator and the custodian, as along with counterparty risk and any associated fees.

Pooled and liquid staking: Pooled staking lowers the entry barrier and offers liquidity through tradable tokens but introduces smart contract, market, and potential depegging risks if the liquid staking token trades below the value of the underlying asset.

The rewards of staking

Staking offers investors the ability to earn income on crypto assets intended to be held for the long-term. That being said, rewards are not fixed like interest payments on a bond (Exhibit 2). They vary over time, shaped by a number of factors, including the network’s economic design (token issuance schedules, transaction fees, slashing), the size of the validator set, and market activity (transaction demand and maximum extractable value opportunities).[6]

Exhibit 2: Staking reward rates vary across tokens and over time

Ethereum

Rewards depend on how many validators are active: the more validators there are, the more the newly issued ETH is spread out, so the annual percentage return (APR) on staking for each validator goes down.

In addition to issuance, validators also earn transaction fees and potentially MEV, which can boost returns during periods of elevated network activity.

Solana

Rewards are derived from token inflation, transaction fees, and priority fees paid by users during periods of high network demand.

Validators may also capture MEV by using Jito software. Whether this extra revenue is shared with delegators depends on each validator’s policy.

The risks of staking

Price volatility: Staking rewards are typically modest when compared with the underlying token’s price fluctuations, which remain the primary driver of both risk and potential return in most crypto asset investments.

Slashing: Failure to adhere to the network’s rules—such as being offline or attempting to validate fraudulent transactions—can result in penalties, up to and including the loss of a portion of the staked ETH, a process known as “slashing.”

Lock-up period: Investors who stake their tokens have limited liquidity during staking, which can impact portfolio rebalancing and the ability to respond to market changes.

Smart contract risk: Investors face the possibility of vulnerabilities or exploits in the underlying staking protocol or smart contracts, particularly on less secure or experimental networks.

Conclusion

Staking is not just income—it is a critical part of the digital asset economy. It aligns incentives among participants and secures blockchains. It also provides rewards for investors, protocols, and service providers by offering a structurally distinct source of income for digital asset portfolios. Staking is infrastructure for the digital asset system and is the backbone of the economic model on the blockchain.

Index definitions: FTSE/Grayscale Crypto Sectors total market index. CoinDesk Composite Ether Staking Rate (CESR) is a daily benchmark rate that represents the mean, annualized staking yield of the Ethereum validator population.

[1] In the 180 days ending September 28, 2025, the Ethereum staking reward rate averaged 2.98% based on the CoinDesk Composite Ether Staking Rate (CESR).

[2] Source: Artemis, Coingecko, FTSE/Russell, Grayscale Investments. Share of PoW assets based on top 20 PoW networks by market cap according to Coingecko. Share of total crypto market capitalization based on FTSE/Grayscale Crypto Sectors total market index. Data as of September 30, 2025. For illustrative purposes only.

[3] Rewards are not guaranteed in every instance — they are expected outcomes for validators who perform duties correctly. Each proof of stake network defines its own reward schedule and inflation mechanics, but actual payouts depend on factors like validator uptime, proper performance, and the total amount staked on the network. For example, if a validator goes offline or fails to submit blocks, they may receive reduced rewards or none at all. So while the protocol is designed to reward good behavior with additional tokens, the guarantee is conditional on validators fulfilling their responsibilities consistently.

[4] Source: Artemis, Coingecko, Grayscale Investments. Based on 20 largest PoS assets according to Coingecko, excluding HASH. Data as of September 29, 2025. For illustrative purposes only.

[5] Ethereum does not natively support delegation; instead, holders participate through staking pools or liquid staking protocols.

[6] Maximum extractable value (MEV) refers to additional rewards that may be available from optimal block construction; MEV rewards are distinct from staking rewards.

Share This

Like what you see?

Subscribe below for the latest research from Grayscale.