Last Updated: 3/20/2025 | 28 min. read

Along with Linux, Python, and a handful of other examples, Ethereum can be considered one of the most important open-source software projects of all time. Although less than 10 years old, today the Ethereum network consists of more than 11,000 nodes, processing 35-40 million transactions every month, securing approximately $46bn in value, and benefiting from the support of more than 2,100 full-time developers. The broader Ethereum ecosystem of interconnected blockchains now processes around 400 million transactions per month.[1]

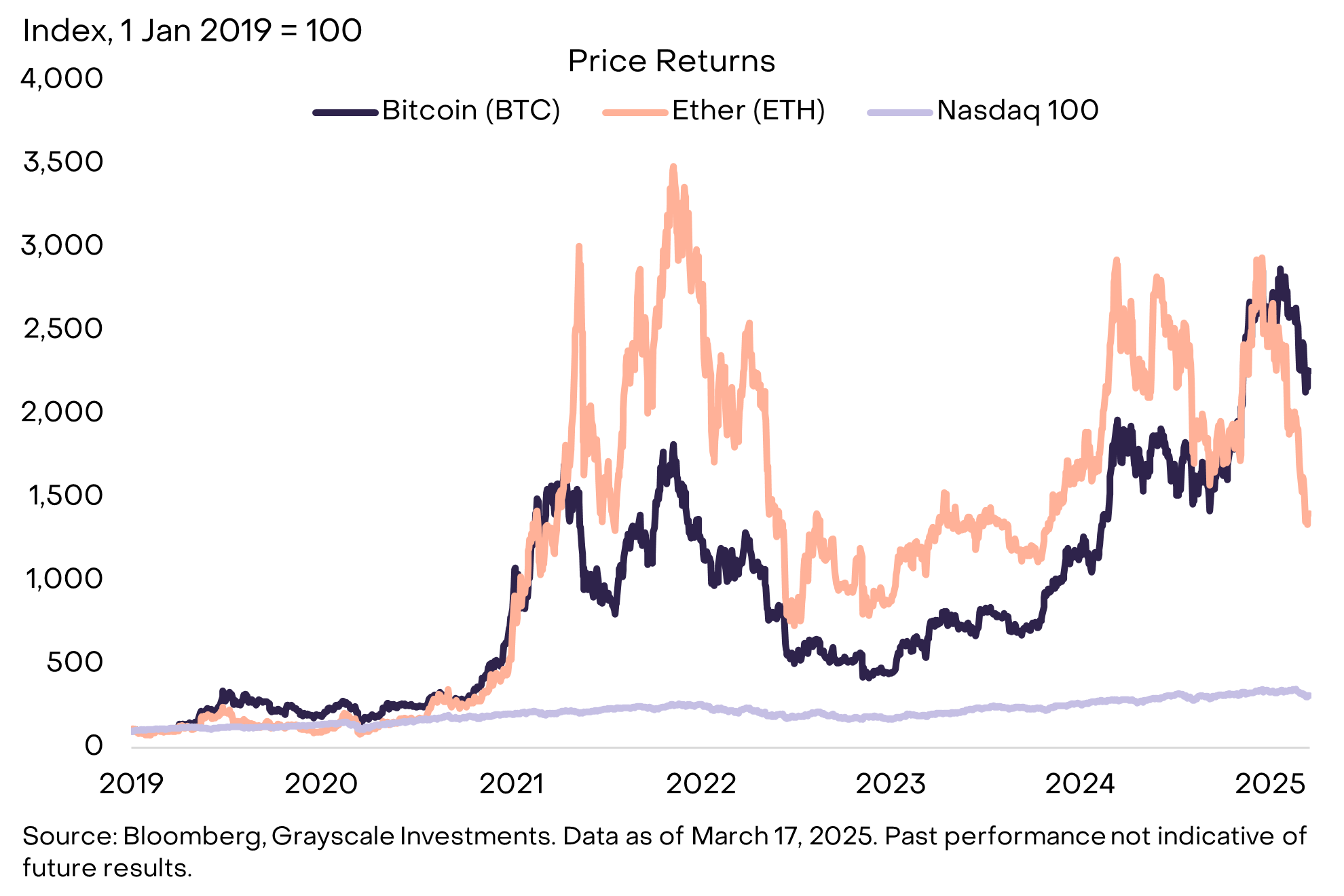

Despite its position in the crypto industry — as well as the launch of spot-based exchange-traded products (ETPs) last year — the market value of the Ethereum network’s Ether (ETH) token has significantly lagged Bitcoin (BTC). In fact, the ETH/BTC price ratio has fallen back to levels last seen in mid-2020 (Exhibit 1). In market value terms, since the end of 2022, Ether’s market cap has increased by about $90 billion while Bitcoin’s market cap has increased by about $1.35 trillion (i.e., about 15 times more).[2] Ether has also recently underperformed the tokens of certain other smart contract platforms, including Solana and Sui.

Exhibit 1: Ether has underperformed Bitcoin for 2-plus years

The sustained underperformance has led some observers to begin questioning the outlook for Ethereum network activity and the value of the Ether token. Although there is uncertainty around the outlook for every crypto asset, we continue to think that Ether should be considered an essential ingredient in diversified crypto portfolios.

Ethereum is not directly comparable to Bitcoin. Bitcoin the network is a monetary system and Bitcoin the asset is used primarily as a medium of exchange and store of value. For those reasons it is part of the Grayscale Currencies Crypto Sector. Bitcoin’s relatively strong price returns reflect investor demand for its attributes as a scarce and censorship-resistant form of digital money.

In contrast, Ethereum is a platform for applications and the Ether token provides utility for the users of those applications. Ethereum is part of the Grayscale Smart Contract Platforms Crypto Sector, along with Solana, Stacks, Sui, and many other networks. Despite the promise of smart contract technology, we have yet to see mass adoption of smart contract-based decentralized applications. There are many early success stories — including the growth in stablecoin transactions — but current adoption is very low compared to the vision for smart contract platforms, which are intended to bring much of traditional finance on-chain.

Grayscale Research believes that adoption of smart contract-based applications will accelerate over the next 1-2 years, partly due to U.S. regulatory changes and forthcoming legislation. The Trump administration has already made changes to federal crypto policy that should allow the industry to invest and flourish in the United States.[3] Separately, a bipartisan group of senators introduced the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act. This legislation, which builds on related efforts from the previous Congress, is intended to provide a comprehensive regulatory framework for the issuance of payment stablecoins. Greater regulatory clarity should facilitate increased investment and adoption of blockchain-based applications, resulting in higher on-chain activity (e.g., transactions and fees) and ultimately value accrual for smart contract platform tokens.

After an initial head start, Ethereum now faces meaningful competition from other smart contract platforms, and it will need to execute on its ambitious development plans in order to be successful. But Ethereum also has differentiating features that we expect to be especially valuable for financial uses cases — including a large pool of on-chain capital and design choices that emphasize decentralization and neutrality. We therefore expect that Ethereum will capture a significant share of future on-chain activity, and this in turn will drive value to the Ether token.

Ethereum was the first major smart contract platform blockchain. Just like Bitcoin, the Ethereum blockchain can be used to send and receive transactions. However, with the addition of smart contracts, Ethereum can also run decentralized applications. These applications can be anything from decentralized lending platforms to identity solutions to video games.[4] Because it functions as the infrastructure for applications, Ethereum can be thought of as a software-based computer and is sometimes referred to as the “world computer.”

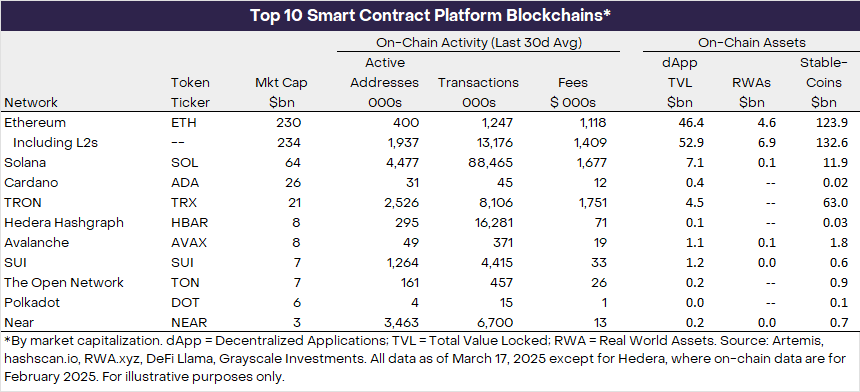

Today Ethereum hosts thousands of applications and is the largest asset in our Smart Contract Platforms Crypto Sector by market cap. Ethereum has more on-chain assets (e.g., stablecoins and tokenized assets) than other leading smart contract blockchains, but it has recently lagged certain other blockchains by measures of on-chain activity (Exhibit 2). Solana, the second-largest network by market cap, had higher activity in terms of active addresses, transactions, and fees over the last 30 days, but has a market cap only 30% of Ethereum’s market cap.

Exhibit 2: Ethereum is the largest smart contract platform by market cap

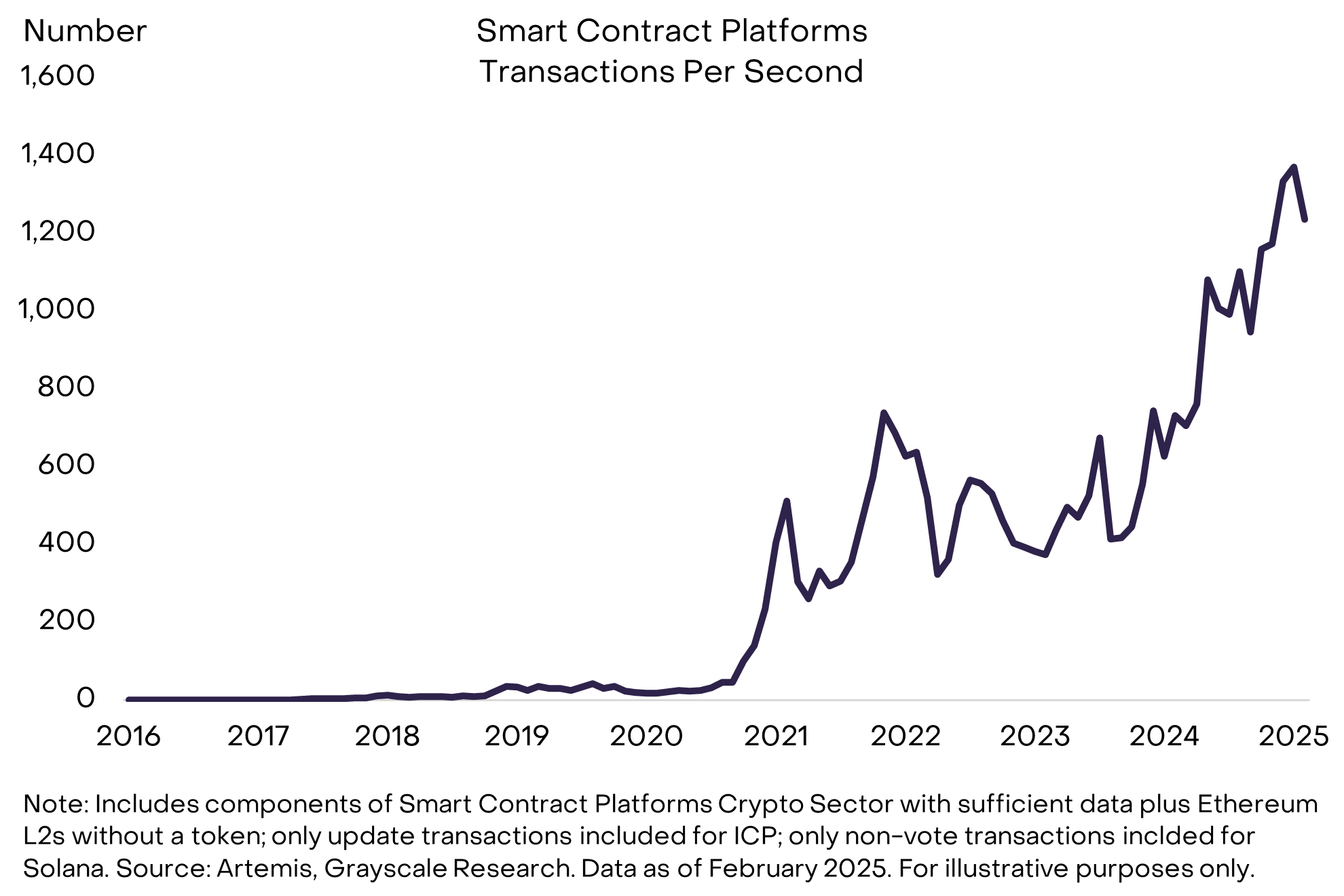

The investment thesis for smart contract platforms is that new applications will result in more users, more transactions, and ultimately more fees for the underlying protocol. We estimate that transaction volume for smart contract platforms has risen from about 20 transactions per second (TPS) five years ago to about 1,200 TPS today, implying an annualized growth rate of about 130% (Exhibit 3). For comparison, in the 12 months ending September 30, 2024, the Visa network processed about 7,400 TPS.[5] If smart contract blockchains can continue to grow as a share of digital payments — and if they can establish competitive moats and maintain pricing power — this will result in rising fee revenue and likely token price appreciation (for more background, see The Battle for Value in Smart Contract Platforms).

Exhibit 3: Smart contract blockchains process ~1,200 transactions per second

Ether has performed broadly in line with its peer group, as measured by the FTSE/Grayscale Smart Contract Platforms Crypto Sector Index (Exhibit 4). This market segment currently includes 70 tokens with an aggregate market capitalization of $428bn.[6] Since the start of 2024, the Smart Contract Platforms index has declined by 22% while Ether’s price has declined by 18%. In contrast, Solana’s price has increased by 18% and Bitcoin’s price has increased by 90%.

Exhibit 4: Ethereum has performed roughly in line with its market segment

Ethereum monetizes network activity through transaction fees — known as “gas fees” — which are payments required to execute transactions or interact with smart contracts. Unlike Solana and many other blockchains, activity in the Ethereum ecosystem takes place both on the Layer 1 (L1) Ethereum mainnet and on a constellation of Layer 2 (L2) networks. This is how Ethereum intends to scale to millions more users, because the L1 itself cannot sufficiently expand capacity without sacrificing decentralization. If working in harmony, this layered structure should offer users the option of high-throughput and low-cost L2 transactions while preserving the security and decentralization of the L1 (for more background, see our report Ethereum’s Coming of Age: “Dencun” and ETH 2.0). However, the migration of activity to L2s has affected the level of distribution of fees across the network, which we explain below.

Gas fees differ structurally between Ethereum’s L1 and L2 networks, reflecting their distinct roles in the protocol’s scaling strategy. Ethereum’s L1 employs a fee model with three distinct components:[7]

For example, the fee for a 1 ETH transfer (which requires 21,000 gas) with a 10 gwei base fee and 2 gwei tip would be:

=21,000*(10+2)=252,000 gwei or 0.000252 ETH

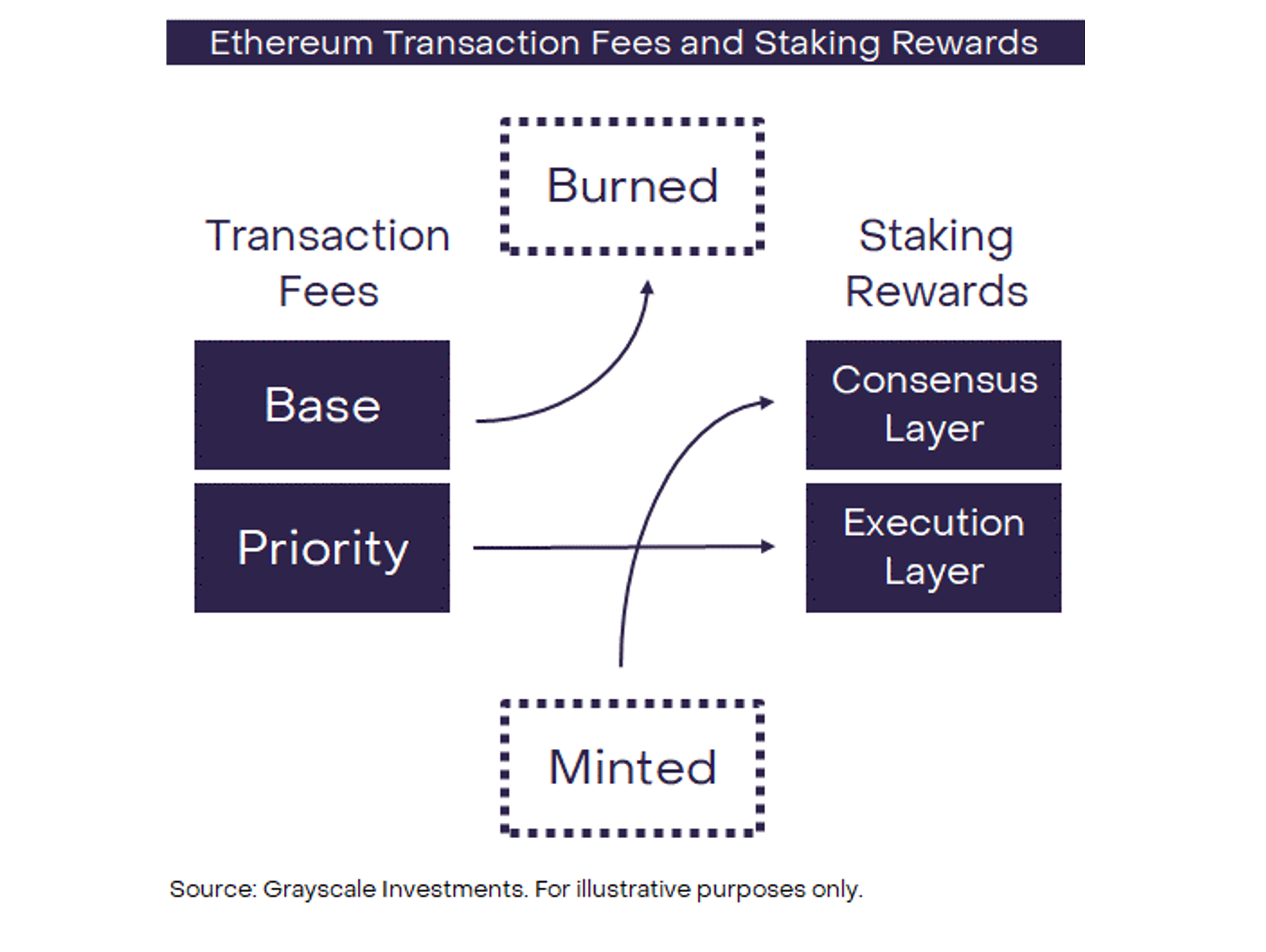

Transaction fees accrue value to token holders through mechanics that resemble dividends and buybacks in equity markets. Priority fees are paid to validators as a part of staking rewards, similar to dividends. Base fees are burned to reduce ETH supply, rewarding all token holders, similar to buybacks. (Exhibit 5).

Exhibit 5: Fees are distributed to token holders through staking rewards and burns

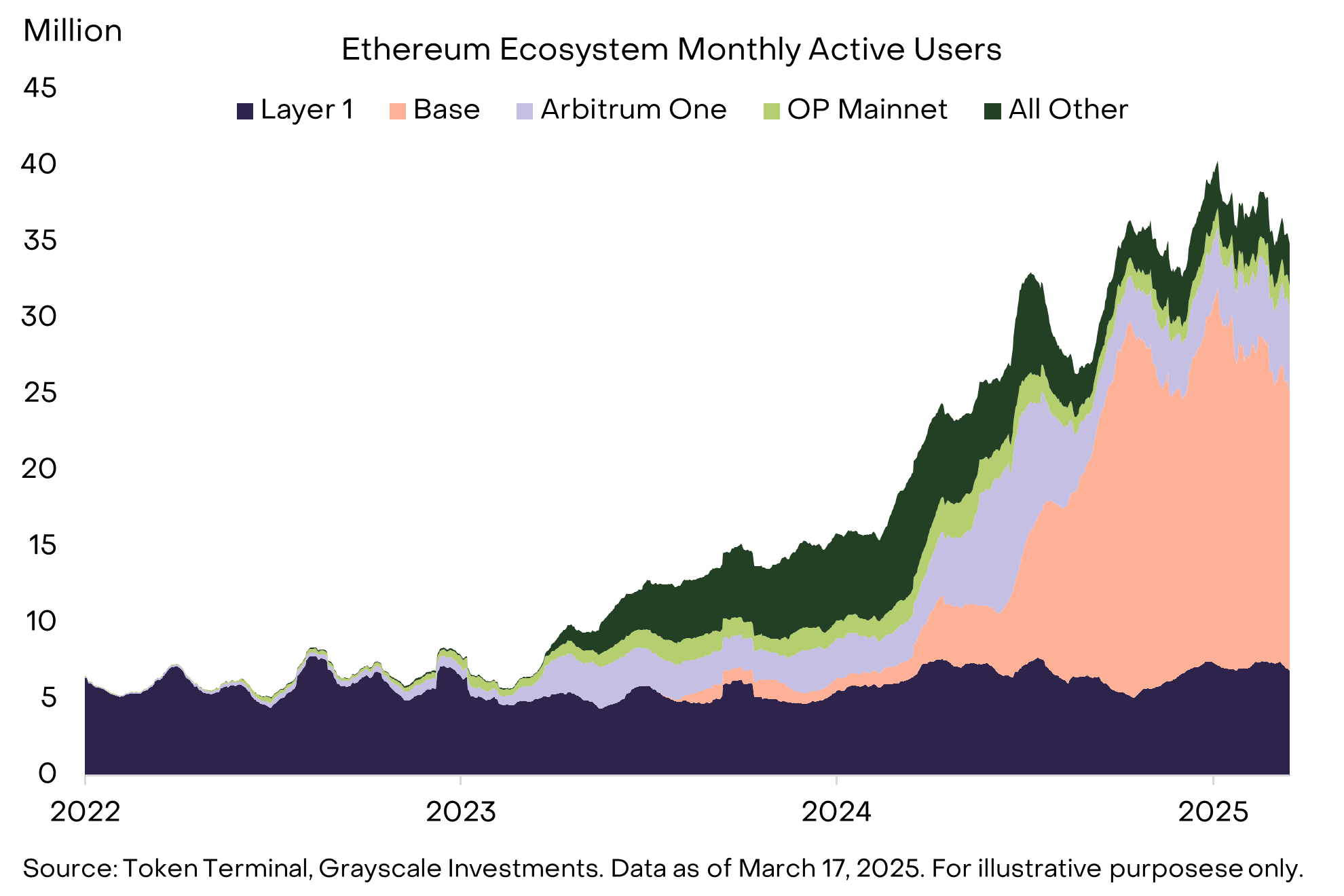

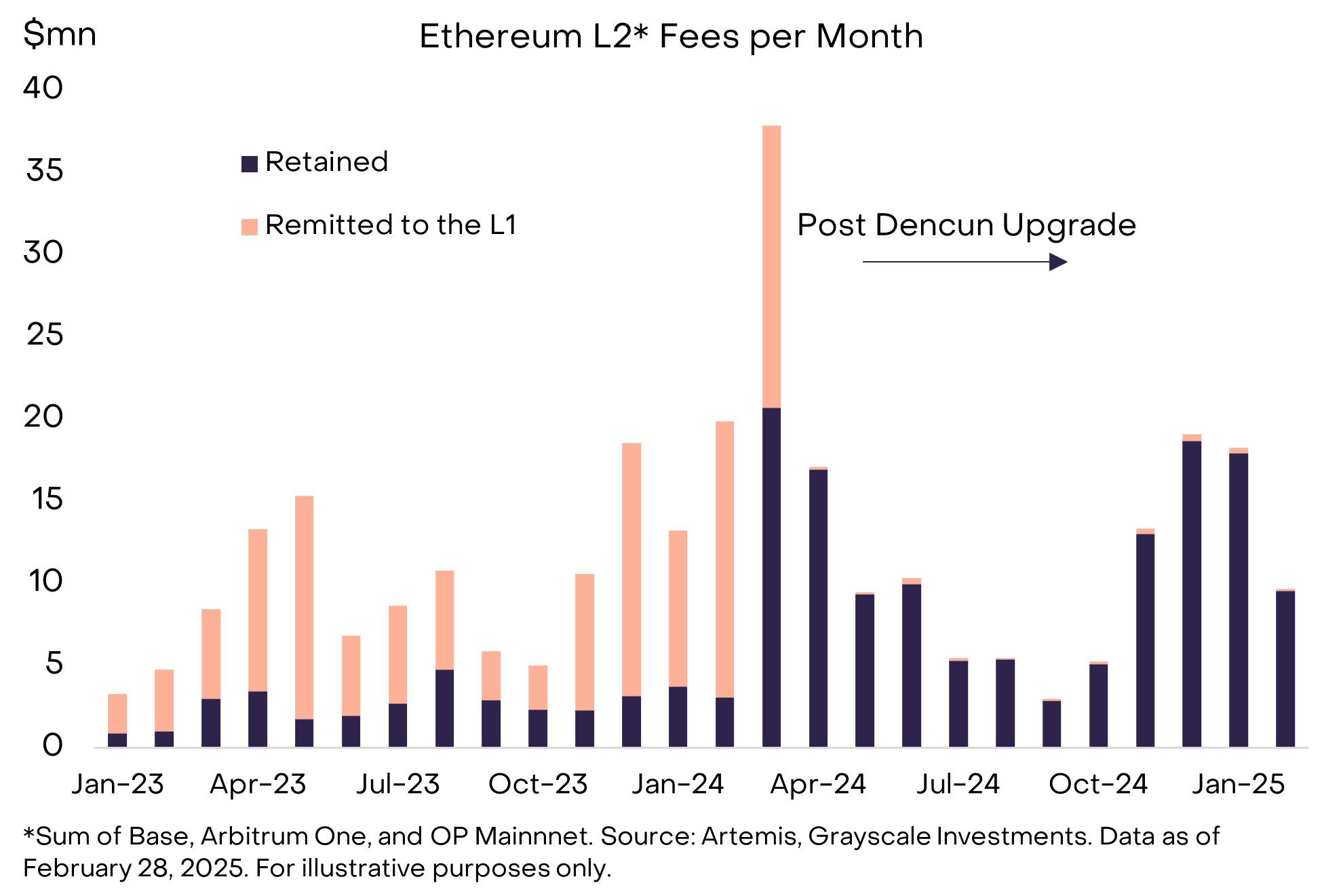

Layer 2 networks like Arbitrum One and Base also charge transaction fees. Because they rely on the Ethereum Layer 1 network for final settlement and security, L2s are able to charge much lower transaction fees and process more transactions per second. However, L2s remit a portion of their fees to the L1 as payment for settlement and security services. Last year Ethereum went through a hard fork (network update) known as Dencun, which was intended to help expand the L2 ecosystem. The Dencun upgrade introduced blob[8] transactions, which are a low-cost way for L2s to post their data to the L1. The upgrade succeeded in significantly increasing the number of users and number of transactions on the L2s (Exhibit 6).

Exhibit 6: Significant growth in activity on Ethereum’s L2s

However, the introduction of blob transactions also affected the level and distribution of fees across the network. Most importantly, blob transactions reduced the amount of fees paid by the L2s to the L1 (Exhibit 7). This has led some observers to argue that L2s are “parasitic” to Ethereum because in the short run the success of L2s comes at the expense of the L1. But if L2s benefit from remaining within the Ethereum ecosystem — like security guarantees and other network effects — then a large ecosystem of L2s will ultimately bring much more value to the Ethereum network and ETH in the long run.

Exhibit 7: Ethereum L2s now paying less to the L1

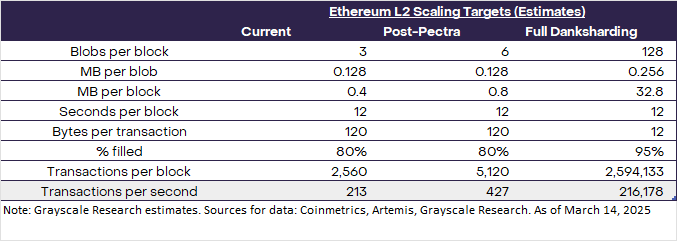

Future upgrades will continue to scale both the L1 and L2s. The Pectra upgrade, scheduled for April 2025, combines Prague (execution layer) and Electra (consensus layer) enhancements. Specifically for scaling, Ethereum Improvement Proposal-7691 optimizes blob storage, targeting 6 blobs/block, doubling the blob capacity of Dencun. Looking ahead, Ethereum’s scaling potential could increase significantly with the implementation of a concept known as Full Danksharding (Exhibit 8).[9] This upgrade involves expanding both the number of blobs per block and the size of each blob, dramatically raising the upper limit of TPS. Exhibit 8 shows Pectra and Full Danksharding could affect the transaction capacity of the Ethereum L2s.

Exhibit 8: Future Ethereum upgrades will greatly increase L2 capacity

The outlook for smart contract platform fees is highly uncertain, partly because the technology is at an early stage, and we do not know how much pricing power platforms like Ethereum will be able to maintain over time. Smart contract platforms compete with one another and also compete with centralized systems. To maintain pricing power in the longer run, they will need to offer differentiating features that prevent users from switching to cheaper (centralized or decentralized) alternatives. Although the Ethereum blockchain is slower and more expensive than many competitors, Grayscale Research believes that its unique advantages — including a high value of on-chain assets and an emphasis on decentralization and security — will contribute to adoption and network effects, and ultimately provide Ethereum with a degree of pricing power over time.

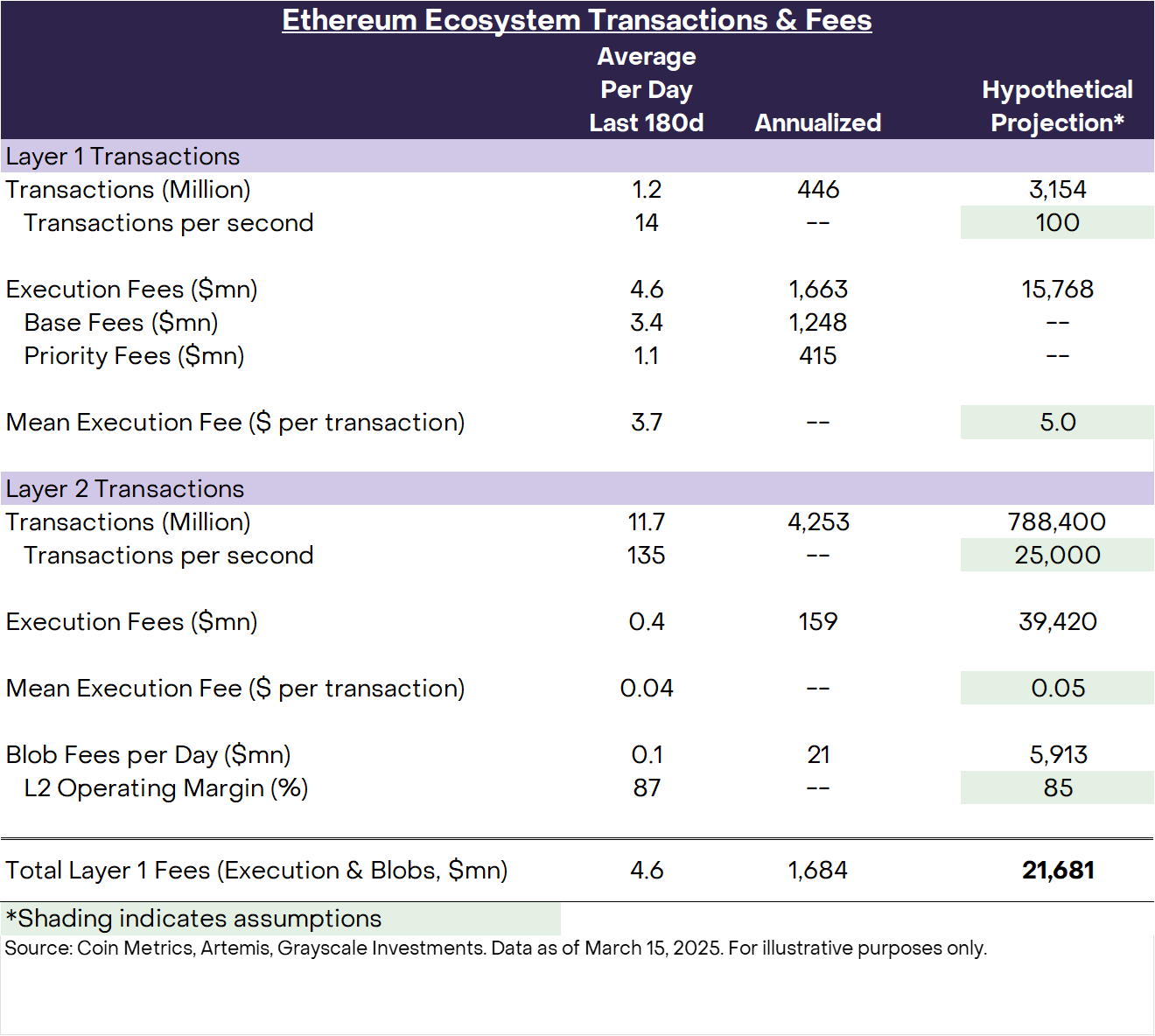

Exhibit 9 shows an illustrative example of how Ethereum could potentially grow fees by increasing capacity and maintaining pricing power. We assume an average transaction fee of $5.00 on the L1 — compared to an average of $6.30 since 2019.[10] In the longer run, the Layer 1 will presumably be used primarily for high-value transactions and those requiring high-security assumptions. For the L2s, we assume an average transaction fee of $0.05, which is also similar to recent experience. We further assume that the Ethereum L1 processes 100 TPS and that the Ethereum L2s collectively process 25,000 TPS. These are hypothetical TPS projections that are achievable within the next 3-5 years under Ethereum’s scaling roadmap and assuming significant growth in overall demand for smart contract-based applications.[11]

Under these assumptions, total Ethereum Layer 1 fees would grow to more than $20bn, from an annualized rate of about $1.7bn over the last six months (Exhibit 9). Although the outlook for fees is highly uncertain, Ethereum should be technically capable of significantly growing fee revenue if it executes on its scaling strategy and maintains some pricing power.To monitor progress, investors should consider tracking the fundamentals variables in this simplified model—namely L1 and L2 TPS and L1 and L2 average execution fees.[12]

Exhibit 9: Ethereum fee revenue can grow with scaling and pricing power

In the last crypto bull market, Bitcoin and Ether initially appreciated in tandem. Then in 2021, Ether’s price moved up more quickly, ultimately delivering a price return roughly two times higher than Bitcoin’s from the start of 2019 to the peak of the market in November 2021 (Exhibit 10). Some crypto investors may have been positioned for a similar pattern in the current cycle — with Ether significantly outperforming as the cycle matured — and have been disappointed by its recent weakness.

Exhibit 10: Last crypto cycle Ether eventually outperformed Bitcoin

Grayscale Research sees Ether’s underperformance as a healthy sign that crypto markets are focused on fundamentals. In our analytical framework, crypto markets differentiate smart contract platforms primarily on the basis of fees.[13] Although fees do not translate into token value accrual in exactly the same way across blockchains, they are typically passed to token holders, and fees are arguably the most directly comparable measure of blockchain activity.

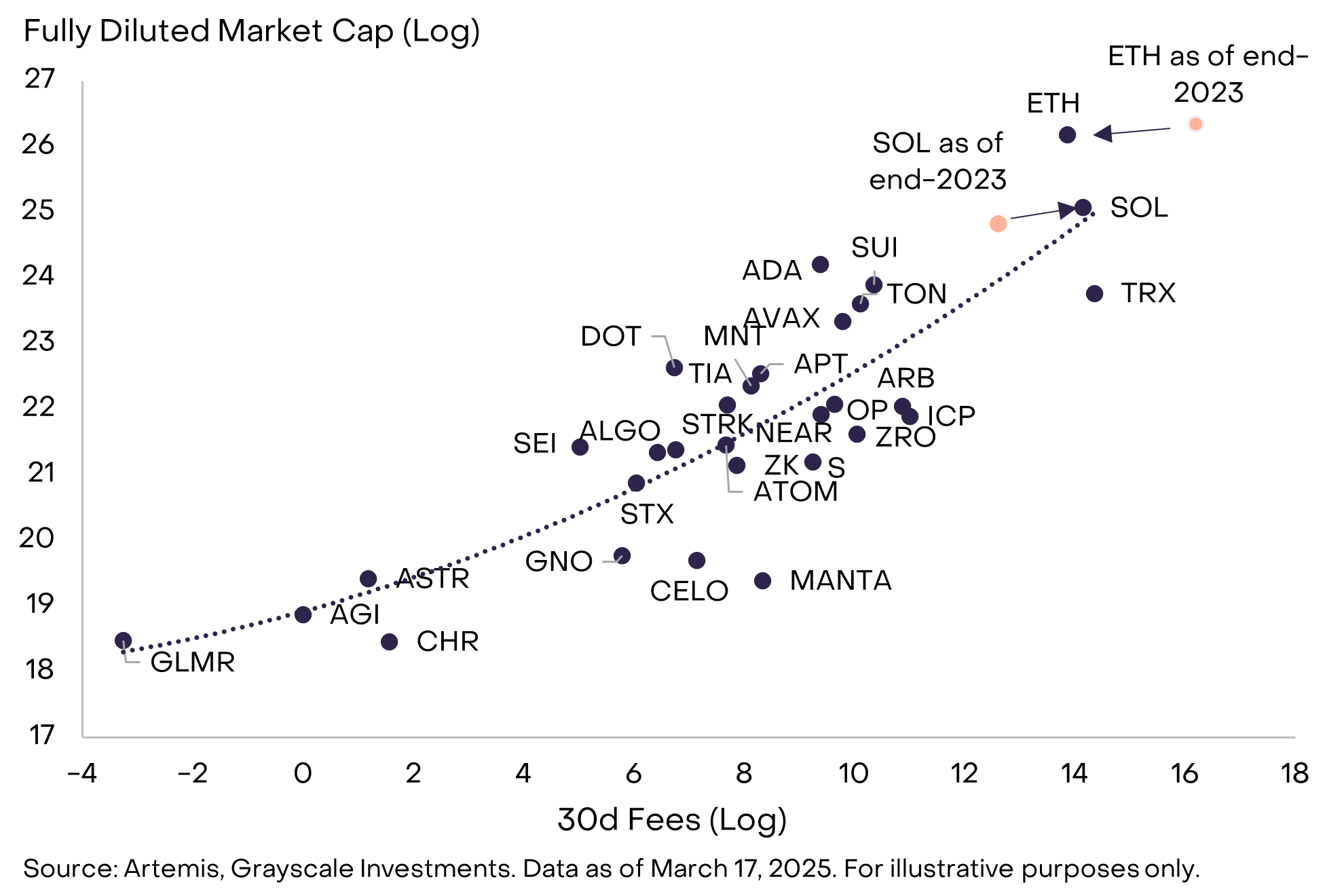

Within the Smart Contact Platforms Crypto Sector, both Ethereum and Solana have relatively high fees and market caps (Exhibit 11). Since the end of 2023, Solana has gained fee revenue and market share in the Smart Contract Platforms Crypto Sector, while Ethereum has lost fee revenue and market cap. In other words, markets have appropriately repriced the relative value of Ethereum and Solana due to changes in fundamentals. In the simple framework shown in Exhibit 11, Solana moved up and to the right and today looks roughly fairly valued (it “grew into its valuation”). In contrast, Ethereum moved down and to the left and today may be valued at a premium to its fee revenue.

Exhibit 11: Ethereum underperformed Solana due to weaker fee growth

These small differences in competitive position matter, but not as much as potential growth in the category as a whole. Adoption of all smart contract platforms is at an early stage. For example, Ethereum today only has around 7 million monthly active users, whereas Facebook parent company Meta Platforms reported 3.35 billion “daily active people” on its applications in December 2024.[14] As adoption increases, smart contract platforms are poised to benefit from compounding network effects, where rising participation not only drives higher transaction volumes and fee revenue but also accelerates developer activity, liquidity depth, and interoperability across ecosystems. This reinforcing cycle of adoption and utility could amplify value capture across the entire category.

The winning networks will likely be those that capture the most transaction fees over time and otherwise have favorable structural supply/demand conditions for their native tokens (e.g., due to limited supply growth and structural demand as a collateral asset or payments medium). Solana, Sui, and a few other smart contract platforms will differentiate themselves from competitors with high throughput, low transaction costs, and a generally compelling user experience. Ethereum stands apart due to a large and diverse application and developer ecosystem, a large amount of on-chain capital, and a culture that prioritizes decentralization, security, and neutrality. We expect that these features will continue to draw many users to the Ethereum ecosystem, and that Ethereum will capture a significant share of economic activity on smart contract platform blockchains in the future.

## Investment Opportunities ##

Grayscale offers interested investors a variety of ways to incorporate Ether and/or other smart contract platforms in a portfolio. For Ether, investors should consider the Grayscale Ethereum Mini Trust ETF (ticker: ETH) — the lowest-cost Ethereum exchange-traded product in the U.S.* — as well as the pioneering Grayscale Ethereum Trust ETF (ticker: ETHE) — the first Ethereum trust of its kind.

ETHE and ETH (collectively the "Funds"), exchange traded products, are not registered under the Investment Company Act of 1940 (or the ’40 Act) and therefore are not subject to the same regulations and protections as 1940 Act registered ETFs and mutual funds. An investment in the Funds is subject to a high degree of risk and heightened volatility. The Funds are not suitable for an investor that cannot afford the loss of the entire investment. An investment in the Funds is not a direct investment in Ether.

Ethereum is also the second-largest component of the diversified Grayscale Digital Large Cap Fund (ticker: GDLC).

Eligible accredited investors** interested in broader exposure to smart contract platforms can consider the Grayscale Smart Contract Fund, as well as our single-asset trusts holding Avalanche, Optimism, Near, Solana, Stacks, and Sui.

To learn more about investing with Grayscale, reach out to our portfolio consultants at 866-775-0313 orinfo@grayscale.com.

Glossary

Altcoin: Crypto assets other than Bitcoin.

Blockchain: A distributed digital ledger that securely stores records across a network of computers in a transparent and tamper-resistant manner.

Centralized: A system or organization in which decision making, control, and authority are concentrated in a central point or a small group of entities, often resulting in a single point of failure or authority.

Cryptocurrency (e.g., digital currency): A digital form of currency that uses cryptography for secure and decentralized transactions. Crypto assets power blockchain networks, and serve as incentives for the verification of transactions.

Decentralized Applications ("dApps"): Software applications that run on top of blockchain networks. These applications are digital, decentralized equivalents of apps on a mobile device, and vary from financial to gaming to third party services.

Decentralized Network: A network architecture where control and data are distributed across multiple nodes rather than being managed by a single central authority.

DePIN: Decentralized Physical Infrastructure Networks that use blockchain and token rewards to incentivize individuals to contribute physical infrastructure resources.

Ethereum: A decentralized blockchain platform with smart contract functionality, using Ether (ETH) as its native cryptocurrency.

Internet of Things (IoT): The Internet of Things (IoT) refers to the network of interconnected physical devices, vehicles, appliances, and other objects embedded with sensors, software, and connectivity features, enabling them to collect and exchange data over the internet.

Market Capitalization (or “Market Cap”): Calculated by multiplying the market price of a given crypto asset by the total number of tokens outstanding. Market cap can provide a rough snapshot of the value that investors place on the ecosystem associated with a crypto asset.

Memecoin: A cryptocurrency created for fun or comedic purposes, frequently based on memes or humor, rather than serious technological development.

Non-Fungible Token ("NFT"): A digital asset stored on a blockchain that represents ownership over a distinct, unique item. Dollars or Bitcoin are examples of “fungible” items as each unit is equivalent; conversely every NFT is “non-fungible” as each unit is entirely unique in its characteristics.

Oracle: An external data source that provides real-world information (stock prices, sports outcomes, political polling data) to smart contracts on the blockchain.

Protocol: A set of rules and conventions, embedded in code, that govern a blockchain network.

Smart Contract: Software that functions as a self executing contract with predefined rules and conditions that automatically executes on a blockchain.

Smart Contract Platform: A blockchain designed primarily for executing decentralized applications (“dApps”) run on smart contracts.

Solana: A crypto computing platform designed to achieve high transaction speeds without sacrificing decentralization, using innovative approaches like the "proof of history" mechanism.

Staking: The process of locking up cryptocurrency as collateral to support network security in return for earning tokens.

Token: In the context of cryptocurrency, a token is a digital representation of an asset that has been created on an existing blockchain, often used to represent ownership in a specific platform or ecosystem. Tokens can serve various functions, including as a medium of exchange, a store of value, or a representation of voting rights within a decentralized system.

Token rewards: Incentives given in the form of cryptocurrency tokens to participants in a blockchain network for their contributions or activities.

Web3: The next phase of the internet, powered by blockchain and decentralized technologies, aiming to create a user centric and trustless digital environment where individuals have more control over their data, interactions, and the platforms they spend their time and money on. Also known as Web 3.0.

Zero Knowledge Proof (“ZK Proof”): A cryptographic practice that uses mathematical proofs to prove the validity of a transaction without providing additional identifying information to either transacting party. ZK proofs are one of the measures employed by certain blockchains to prioritize user anonymity and privacy.

*ETH is low cost based on gross expense ratio at 0.15%.

**Grayscale’s private placements are only available to Accredited Investors as defined in Rule 501(a) of Regulation D under the Securities Act of 1933, as amended. Most individuals are not Accredited Investors. For additional information, please consult https://www.sec.gov/newsroom/speeches-statements/spch121714laa.

[1] Source: Nodewatch.io, Artemis, DeFi Llama, Electric Capital, Grayscale Investments. All data as of March 17, 2025 except number of developers, which is as of November 2024. Total ecosystem transactions include the following L2s: Base, Arbitrum One, OP Mainnet, ZKsync Era, Starknet, Blast, Linea, Scroll, and World Chain.

[2] Source: Artemis, Grayscale Investments. Data as of March 17, 2025.

[3] For more information, see January 2025: Remake of U.S. Crypto Policy Underway and February 2025: Progress, Potholes, and Opportunity, Grayscale.com.

[4] For more background, see The State of Ethereum and Layer 1 Blockchains: A Tale of User-Owned Cities Part 1 and Part 2, Grayscale.com

[5] Source: Visa Annual Report 2024, Grayscale Investments. Visa processed 233.8 billion transactions in its fiscal year or about 7,400 per second.

[6] Source: FTSE/Russell, Artemis, Grayscale Investments. Data as of March 17, 2025.

[7] Market Byte: The Merge, September 24, 2022, Grayscale.com.

[8] An Ethereum blob is a temporary data storage unit (retained for ~18 days) used by Layer 2 networks to efficiently batch off-chain transaction data while leveraging Ethereum's security, reducing fees by ~90% compared to permanent on-chain storage.

[9] Danksharding, Ethereum Roadmap, Ethereum.org.

[10] Source: Coin Metrics, Grayscale Investments. Data as of March 15, 2025.

[11]The TPS assumptions are not theoretical maximums.

[12] L2 operating margins, or the portion of execution fees that are retained by the L2, could also change in the future, but that is beyond the scope of this report.

[13] In this report we have excluded a discussion of the “money premium” (if any) in token valuations. See The Battle for Value in Smart Contact Platforms, Grayscale.com.

[14] Source: Token Terminal; Meta Reports Fourth Quarter and Full Year 2024 Results, Meta Investor Relations.

ETP Disclosures:

Grayscale Ethereum Trust ETF (“ETHE” or the “Fund”) has filed a registration statement (including a prospectus) with the SEC for its offering to which this communication relates. Before you invest, you should read the prospectus in such registration statement and other documents the Fund has filed with the SEC for more complete information about such Fund and its offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the Fund or any authorized participant will arrange to send you such prospectus (when available) if you request it by emailing info@grayscale.com or by contacting Foreside Fund Services, LLC, Three Canal Plaza, Suite 100, Portland, Maine 04101.

Please read the prospectus carefully before investing in ETH. Foreside Fund Services, LLC is the Marketing Agent for the Funds.

Grayscale Digital Large Cap Fund (“GDLC”) Disclosures:

Grayscale Digital Large Cap Fund LLC may file a registration statement(including a prospectus) with the SEC for the offering to which this communication relates. Before you invest, you should read the prospectus in that registration statement and other documents GDLC has filed with the SEC for more complete information about GDLC and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, GDLC or any authorized participant will arrange to send you the prospectus after filing if you request it by emailing info@grayscale.com or by contacting Grayscale Securities, 290 Harbor Drive, Stamford, CT06902.

GDLC is speculative and entails a high level of risk. GDLC is not suitable for any investor that cannot afford loss of the entire investment.

Private Placement Disclosures:

Grayscale Operating, LLC (“GSO”) is the parent holding company of Grayscale Advisors, LLC (“GSA”), an SEC-registered investment adviser, as well Grayscale Securities, LLC (“GSS”), an SEC-registered broker/dealer and member of FINRA, and Grayscale Investments Sponsors, LLC ("GSIS", together with GSO, GSS, and GSA, "Grayscale"). GSIS is not registered as an investment adviser under the Investment Advisers Act of 1940 and none of the investment products (“Products”) sponsored or managed by GSIS are registered under the Investment Company Act of 1940.

Private placement securities are speculative, illiquid, and entail a high level of risk, including the risk that an investor could lose their entire investment. The Products are not suitable for any investor that cannot afford loss of the entire investment.

Carefully consider investment objectives, risk factors, fees and expenses before investing. This and other information can be found in each Product’s private placement memorandum, which may be obtained from Grayscale and, for each Product that is an SEC reporting company, the SEC’s website, or for each Product that reports under the OTC Markets Alternative Reporting Standards, the OTC Markets website. Reports prepared in accordance with the OTC Markets Alternative Reporting Standards are not prepared in accordance with SEC requirements and may not contain all information that is useful for an informed investment decision. Read these documents carefully before investing.

The shares of each Product are not registered under the Securities Act of 1933, the Securities Exchange Act of 1934 (except for Products that are SEC reporting companies), the Investment Company Act of 1940, or any state securities laws. The Products are offered in private placements pursuant to the exemption from registration provided by Rule 506(c) under Regulation D of the Securities Act of 1933 and are only available to accredited investors. As a result, the shares of each Product are restricted and subject to significant limitations on resales and transfers. Potential investors in any Product should carefully consider the long-term nature of an investment in that Product prior to making an investment decision. The shares of certain Products are also publicly quoted on OTC Markets and shares that have become unrestricted in accordance with the rules and regulations of the SEC may be bought and sold throughout the day through any brokerage account.

Grayscale does not store, hold, or maintain custody or control of any Product’s digital assets, but instead has entered into a Custodian Agreement on behalf of each Product with a third party custodian to facilitate the security of each Product’s digital assets. The custodian controls and secures each Product’s digital asset account, a segregated custody account to store private keys, which allow for the transfer of ownership or control of the digital asset, on each Product’s behalf. If the custodian resigns or is removed by Grayscale or otherwise, without replacement, it could trigger early termination of such Product.

Risk Disclosures

Extreme volatility of trading prices that many digital assets have experienced in recent periods and may continue to experience could have a material adverse effect on the value of the Product and the shares of each Product could lose all or substantially all of their value.

Digital assets represent a new and rapidly evolving industry. The value of the Product shares depends on the acceptance of the digital assets, the capabilities and development of blockchain technologies and the fundamental investment characteristics of the digital asset.

Digital asset networks are developed by a diverse set of contributors and the perception that certain high-profile contributors will no longer contribute to the network could have an adverse effect on the market price of the related digital asset.

Digital assets may have concentrated ownership and large sales or distributions by holders of such digital assets could have an adverse effect on the market price of such digital assets.

The value of the Product shares relates directly to the value of the underlying digital asset, the value(s) of which may be highly volatile and subject to fluctuations due to a number of factors.

A substantial direct investment in digital assets may require expensive and sometimes complicated arrangements in connection with the acquisition, security and safekeeping of the digital asset and may involve the payment of substantial acquisition fees from third party facilitators through cash payments of U.S. dollars.

Because the value of the Shares is correlated with the value of digital asset(s) held by the Product, it is important to understand the investment attributes of, and the market for, the underlying digital asset. Please consult with your financial professional.

This information should not be relied upon as research, investment advice, or a recommendation regarding any products, strategies, or any security in particular. This material is strictly for illustrative, educational, or informational purposes and is subject to change.

The shares of each Product are not registered under the Securities Act of 1933 (the "Securities Act"), the Securities Exchange Act of 1934 (except for the Products that are SEC reporting companies), the Investment Company Act of 1940, or any state securities laws. The Products are offered in private placements pursuant to the exemption from registration provided by Rule 506(c) under Regulation D of the Securities Act and are only available to accredited investors. As a result, the shares of each Product are restricted and subject to significant limitations on resales and transfers. Potential investors in any Product should carefully consider the long-term nature of an investment in that Product prior to making an investment decision. The shares of certain Products are also publicly quoted on OTC Markets and shares that have become unrestricted in accordance with the rules and regulations of the SEC may be bought and sold throughout the day through any brokerage account.

The Products are distributed by Grayscale Securities, LLC (MemberFINRA/SIPC). SIPC coverage does not apply to the crypto asset products or services mentioned.

© 2025 Grayscale. All rights reserved. The GRAYSCALE and GRAYSCALE INVESTMENTS logos, graphics, icons, trademarks, service marks, and headers are registered and unregistered trademarks of Grayscale in the United States.